Laura Gerhard

Vice President

OVERVIEW

The monthly ABC Position Report exceeded expectations for the third month in a row and posted the best shipment number of the crop season thus far, setting a new industry record for the month. May shipments were 257 million lbs, a 17.4% increase versus the 219 million lbs shipped last year. Domestic shipments came in at 64 million lbs, down 8.2% versus prior year, but consistent with the shipment range seen this crop season. Export shipments also set new record for the month at 193 million pounds. Year-to-date shipments now stand at 2.185 billion lbs, 10.7% behind last year.

SHIPMENTS

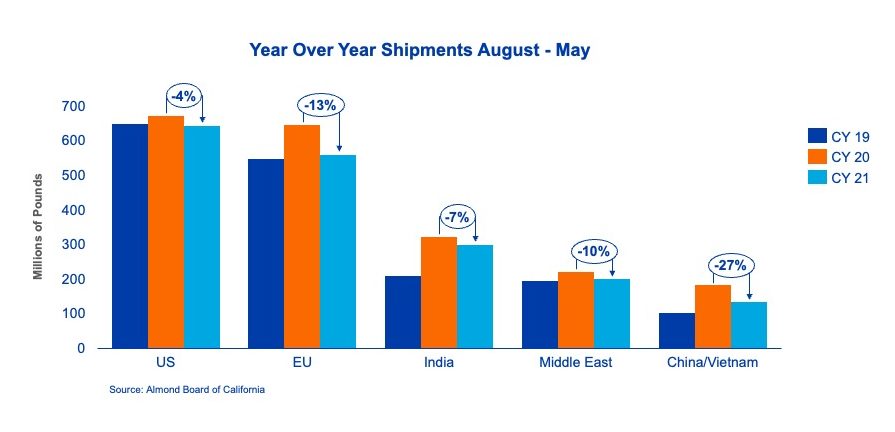

India: Shipments to India were 33.9 million lbs for the month of May compared to 14.1 lbs last year. These strong shipments will temper demand for the short term. Total year-to-date shipments have surpassed 300 million lbs and are now 7% behind last year.

Australian crop quality issues due to a wet harvest combined with a shorter supply estimate will support the need for California almonds. While the Indian trade is filling pipelines for Diwali season, other festivals and daily consumption will continue to drive demand throughout the year.

China: Shipments to China came in at 6.4 million lbs, down 28% compared to last year. Year-to-date shipments continue to trail last year now down 27%. Demand remains challenged due to COVID-related restrictions and effects from inflation. This market will need to replenish stocks in preparation for Chinese New Year; however, buyers are likely to remain conservative in the near term. Many will closely watch demand and consumption for the Autumn Moon Festival at the end of the summer to gauge the strength of consumer demand this fall.

Europe: Shipments to Europe were a robust 74.6 million lbs for the month, up 31% versus the prior season. However, year-to-date shipments trail last year by 13%. Similar to last season, heavy shipments in the spring and summer continue to assure supply for fall and winter months. The market appears well covered for the remainder of the calendar year with limited appetite to take further coverage. The Ukraine crisis, a strong dollar and inflationary pressures have many buyers continuing to show concern regarding consumer demand in the coming months.

Middle East: Shipments to the Middle East were up 10% for the month of May compared to last year as the industry continues to execute on shipments into the region. The strong April and May shipments will provide a much-needed boost in supply as the market heads into Hajj and Eid ul-Adha.

Domestic: Domestic shipments were 64.1 million lbs for the month of May, an 8% decline versus last year. While total shipments were in the monthly range for the year, it suggests continued challenges in demand and the overall supply chain domestically. Global ingredient sourcing has complicated food manufacturer’s ability to produce product as planned. Recovery in certain segments such as foodservice appears to have plateaued, and inflationary pressures are impacting consumer demand.

COMMITMENTS

Total committed shipments now stand at 614 million lbs, up 1% from last May. New sales for the current crop have started to tail off as evidenced by 117 million lbs of new sales versus 103 million lbs last year. Uncommitted inventory remains elevated at 660 million lbs, 52% higher than this time last year. Sold and shipped as a percent of total supply is at 81% vs 88% last year. Vessel shipping execution over the remaining two months of the crop year will be critical to managing the carryout.

The May shipment report provides the first look at commitments for next crop year. Commitments for the 2022 crop season showed 128 million lbs already committed which is down 44% to last season’s 231 million lbs of new crop commitments.

CROP

Crop receipts for the month were 5.4 million pounds. The crop now sits at 2.91 billion pounds. Pollenizer inventories appear more abundant while Nonpareil is in shorter supply, maintaining the price spread between the two at higher levels.

| Market Perspective May shipments exceeded market expectations turning in a crop year high for the third straight month. Export shipments continue to lead the way turning in a record for the second month in a row as the industry continues to find success executing container bookings. The industry is determined to sustain the shipping momentum of recent months and continue to work through the shipment backlog. Price overall remains steady at affordable levels. Market activity for the month remained subdued as sellers and buyers alike mainly focus on executing existing contracts. Demand uncertainty persists as the world economy grapples with inflation, increased energy costs and a strong US dollar. Good progress has been made on drawing down the carryout and will remain the focus to close out the crop year. The market now turns its attention to the 2022 crop. The USDA-NASS Objective Estimate will be released on July 8 which will set the tone and expectations for marketing the new crop. |

To view the entire detailed Position Report from the Almond Board of California Click Here

The following reports may be of interest to you:

Related posts:

ALMONDS SHIPMENT REPORT USA

ALMONDS SHIPMENT REPORT USA  Global Statistical Review, Almonds

Global Statistical Review, Almonds  Iran Almonds: Reduction of almond production in the gardens of Eqlid and Bavanat cities in Fars province

Iran Almonds: Reduction of almond production in the gardens of Eqlid and Bavanat cities in Fars province  Blue Diamond Almonds Market Update: Starting the Year with Another Record Shipment

Blue Diamond Almonds Market Update: Starting the Year with Another Record Shipment  ALMOND SHIPPING REPORT +207 MILLION POUNDS ++7.4%- NEW RECORD

ALMOND SHIPPING REPORT +207 MILLION POUNDS ++7.4%- NEW RECORD  Indian Almond market Increased

Indian Almond market Increased  India: Almond market increased

India: Almond market increased  ALMOND SHIPMENT REPORT-+229 million pounds ++27.3%

ALMOND SHIPMENT REPORT-+229 million pounds ++27.3%