After a long wait, President Erdoğan published the state-guaranteed purchase price for hazelnut kernels in the shell by TMO on Wednesday evening. Levantine grade kernels will be offered TRY 26.50/kg, and Giresunder grade kernels will be offered 27.00/kg. This is roughly in line with the expectations of most major sellers. Accordingly, the announcement did not trigger many reactions in the market, except for some relief, as earlier in the week, there were still rumours that a price of 28 TRY/kg was under discussion. Most of the early pre-sales mean a minus business for the sellers because at that time, one had not yet estimated the bid in such a way, and one had also bet on a further decline of the Turkish Lira. Therefore, one is now glad that it did not come worse.

Although the TMO bid is now on the table, exactly how the season will continue is unclear. On the one hand, the modalities of the TMO are not yet known. It can be seen whether “aggressive” purchasing is intended or whether they only want to set a guideline with the bid and are not actually interested in physical goods.

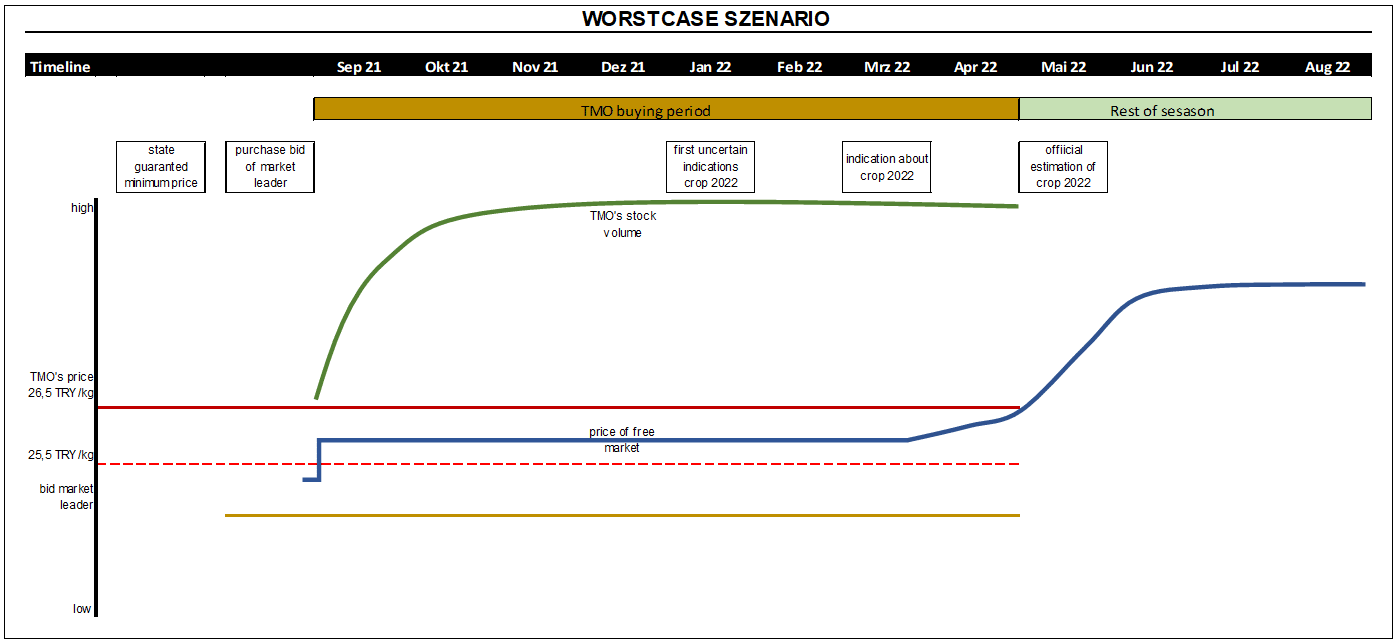

In addition, a decisive point is still to be determined, namely the purchasing bid of the market leader. This will have a significant impact on how prices develop over the course of the season. In principle, there are two scenarios here. If the market leader sets the purchase bid too low, farmers will give some of the product to the TMO. Experience has shown that it was not beneficial for prices if the TMO had an stk to “play politics”. So the worst-case scenario would be that the TMO comes into possession of large stocks, and we get a negative forecast for the 2022 crop in the spring. Then, commodity prices in the range of 28 – 30 TRY/kg would be quite realistic.

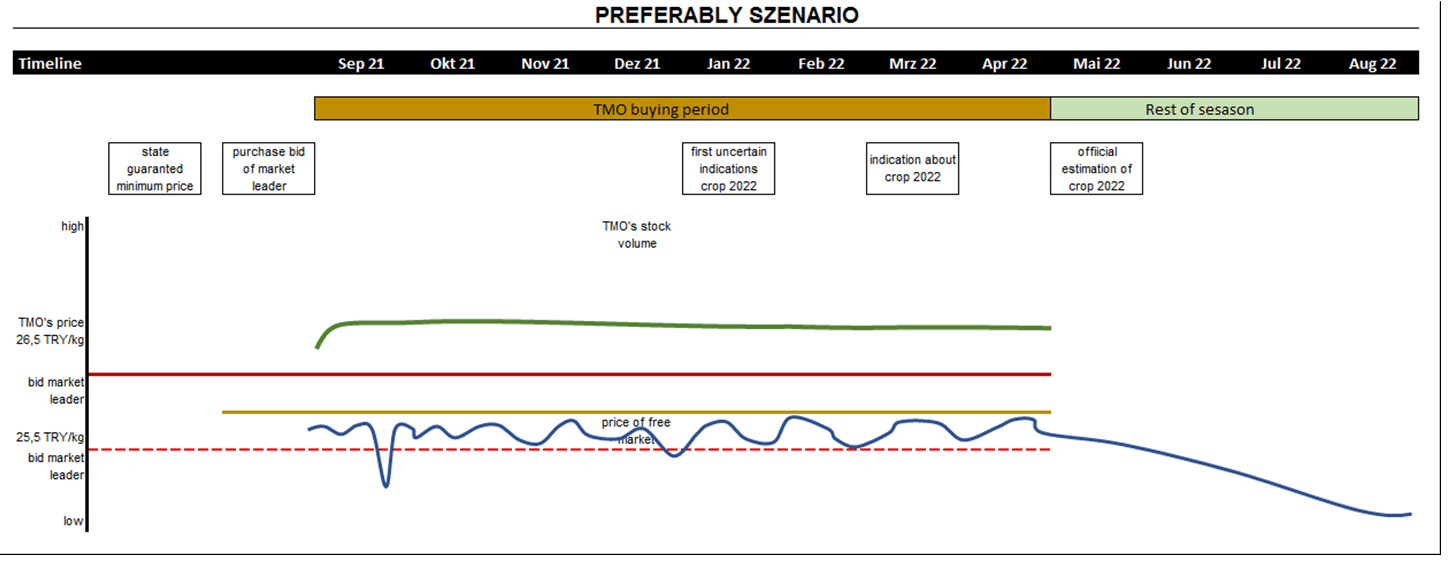

However, the market’s wish would be for the market leader to base its purchase bid relatively close to the purchase bid of the TMO. Experience has shown that the free market has settled around 0.5 to the max. 1.0 TRY/kg below the TMO’s buying bid. If the purchase bid were close to the TMO’s bid, it would not be very lucrative for the local crackers, but they would give quantities to the market leader without much effort.

A fast flow of volumes in the market is also desirable because we have a situation this season that most farmers are satisfied with the prices and want to sell quickly. Still, the small traders and crackers are not interested in financing the expensive stocks expensively. This year, the high level of interest rates again prevents the speculative tendency of these value-creation stages, which is definitely positive. This can also lead to the fact that we will always have positions in the market that are sold cheaply because, just again, someone needs liquidity. Strong this season will be the participants who hardly need financing or the exporters who have the advantage of export credits.

We advise you to watch the market permanently in the coming weeks. In the last years, we had short periods of time at the beginning of the harvest when the prices of raw materials dropped up to 2 TRY/kg below the market price due to short term oversupply (many farmers deliver at the same time). However, this was usually only an effect of 1-2 days.

In principle, however, two-thirds of the season is predetermined by the bid in a certain corridor. The point that will determine whether the last third of the season will be buyer-friendly is, on the one hand, the stock quantity of the TMO, as well as the forecast of the harvest in spring 2022. Should this turn out to be at least in the normal range, the prices could then perhaps even come under pressure due to the surpluses.

In addition to all the forecasts about the development of the price of raw materials, it should not be forgotten that the biggest factor of price development for European buyers in recent years has been the development of the exchange rate. While commodity prices have doubled in Turkey in the last 5 years, and there is no end in sight to the trend due to high inflation rates, the Turkish lira, in turn, has only one-third of its value. Whether and how this trend will continue, however, is uncertain. This week, for example, the lira was able to gain slightly again, although these fluctuations are considered normal.

In addition to the outlook for the coming season, one should not forget to look at the current situation. In the coastal regions, the first farmers have begun picking the nuts, but rainfall is hampering the drying process, and there is no stable period of good weather insight for the coming week. Thus, the drying of the kernels will be further delayed. It can therefore be assumed that the first trucks will not be available in Europe until mid-September. The slow drying could also be critical for mycotoxin levels. Therefore, it is important to keep a close eye on the market in the coming weeks from several points of view.

We continue to notice that, despite the set framework conditions, the offers of the various suppliers sometimes differ significantly from one another. This is not the case for natural kernels, but the range is quite large for processed products. In the next few days, most exporters will change the price lists from harvest 2020 to 2021; then, we will see the price jump, which has existed for some time but is still not present with many buyers.