Double Shock Ahead – EU Sugar Faces Harvest Pressure, Ukraine Quotas, and Mercosur Imports

The European sugar market is heading into a period of unprecedented pressure. A very strong beet harvest is expected this autumn, with new campaign offers for Category 2 sugar already below €0.60/kg. From January 2026, Ukrainian imports at ~€0.38/kg FCA (~€0.45/kg DDP) will reset the EU price floor. On top of this, the Mercosur trade deal – potentially applied provisionally by end-2025 – adds ~374,000 t of additional raw sugar quotas. The result: producers’ hopes of achieving >€0.65/kg are unrealistic, while buyers are sitting back and waiting.

📊 Current Market Snapshot (as of 8 Sept 2025)

- ICE White Sugar No.5 (Oct 25): USD 479.70/t (EUR ~436/t)

- ICE Raw Sugar No.11 (Oct 25): 15.63¢/lb

- EU Spot FCA Poland: quoted >€0.55/kg, but little demand

- DDP Germany: ~€0.63/kg, nominal only

- Retail Germany (Aldi/Lidl): €0.72/kg – below wholesale

🌾 EU Beet Harvest Outlook 2025/26

- Excellent crop conditions across Europe.

- Producers face higher output and rising stocks.

- New campaign (Category 2) offers already <€0.60/kg FCA.

- Producer ambitions for >€0.65/kg seen as unrealistic.

🇺🇦 Ukraine Effect (from Jan 2026)

- New EU quota opens in January.

- Current price in Ukraine: €0.38/kg FCA.

- Delivered into the EU: ~€0.45/kg DDP.

- Likely to reset the EU market floor significantly below current spot levels.

🌎 Mercosur Agreement

- Political deal reached Dec 2024; provisional application possible late 2025.

- Sugar concessions:

- 190,000 t duty-free.

- 183,600 t at €98/t tariff.

- In relative terms small (<3% of imports), but psychologically significant, reinforcing the perception of oversupply.

- Adds additional bearish momentum at exactly the wrong time for EU producers.

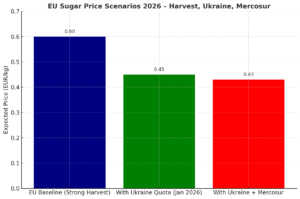

📉 Scenario Analysis – EU Sugar Price Outlook 2026

| Scenario | Expected Price (€/kg) | Comment |

|---|---|---|

| EU Baseline (Strong Harvest) | 0.60 | Already below producers’ €0.65 ambition |

| With Ukraine Quota | 0.45 | Imports reset the market floor |

| With Ukraine + Mercosur | 0.43 | Additional pressure, buyers firmly in control |

🧭 Conclusion & Strategy

📉 Short-term (Q4 2025): Prices fall under harvest pressure, buyers refuse >€0.60/kg.

📉 Medium-term (2026): Ukraine imports reset the market floor to ~€0.45/kg; Mercosur adds symbolic and real pressure.

⚠️ Structural reality: EU producers’ pricing power erodes further; their wish for >€0.65/kg is no longer realistic.

📌 Recommendations:

- Buyers: Sit back and wait – significant downward correction likely from Q4 into 2026.

- Sellers: Secure early contracts before harvest glut and quota inflows; prepare for concessions.

- Traders: Watch for Q1 2026 – Ukraine quota + Mercosur could unleash a double shock, pushing EU sugar prices to multi-year lows.