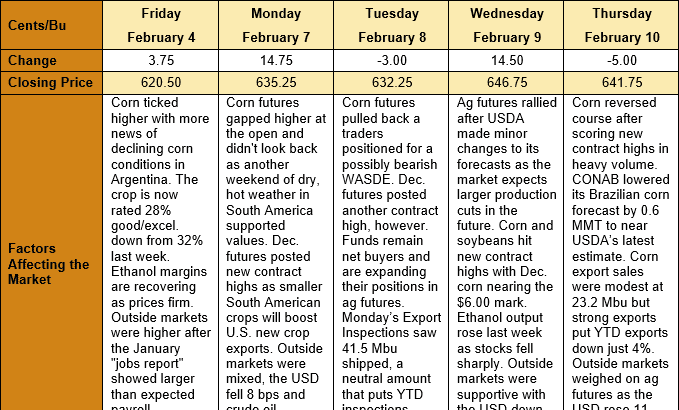

Outlook: March corn futures are 21 ¼ cents (3.4 percent) higher this week after strong rally ended in a possible reversal on Thursday. Futures traded higher heading into and immediately after Wednesday’s WASDE report as demand-rationing concerns outweighed, temporarily at least, the report’s lack of bullish adjustments. Thursday’s trade found profit taking and technical selling that pushed futures off the day’s new contract highs. The market remains focused on the South American crops, but its attention is starting to shift back towards domestic and international demand now that the WASDE is past.

USDA did not make any changes to either the U.S. 2021/22 corn or sorghum balance sheets and made smaller-than-expected adjustments to the South American and world corn outlook. USDA trimmed yield expectations for Brazil’s 2021/22 corn crop fractionally due to the impact of drought on the first crop. USDA is waiting, however, for further development of the safrinha crop (which accounts for roughly 70 percent of Brazil’s production) before making further yield or production cuts. Perhaps most surprising was USDA’s decision to leave the Argentine corn crop estimate unchanged at 54 MMT, which was a significant deviation from pre-report expectations of an 8-MMT cut.

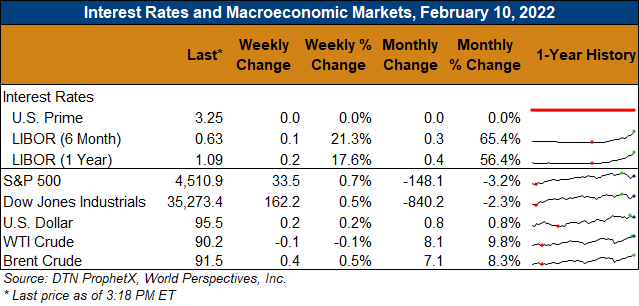

On the world balance sheet, USDA trimmed global production by 1.6 MMT and added small volumes to feed and FSI consumption. Total world consumption was revised 0.94 MMT higher and ending stocks fell 0.85 MMT to 302.2 MMT. The world corn ending stocks-to-use ratio is the tightest since 2013/14, which highlights the need for large South American crops this year.

In complement to USDA’s steady-handed approach to Brazil’s corn production, CONAB, the Brazilian USDA-equivalent, made a slight downward adjustment to its forecast on Thursday. CONAB forecast the Brazilian crop at 112.3 MMT, down 0.6 MMT from its prior estimate.

U.S. exporters booked 1.002 MMT of new corn sales last week but cancellations pushed the net sales figure down to 0.589 MMT. Exports were strong for the week ending 3 February at 1.149 MMT, down just 1 percent from the prior week. YTD exports now total 20.7 MMT, down 4 percent while YTD bookings total 45.7 MMT (down 21 percent).

UDSA also reported 140,000 MT of net sorghum sales last week up 73 percent from the prior week. Sorghum exports rose 28 percent to 158,100 MT, putting YTD exports at 2.244 MMT and YTD bookings at 6.36 MMT (up 7 percent).

From a technical standpoint, March corn futures are trending higher and bullishly scored new contract highs on Wednesday and Thursday. Thursday’s trade, however, formed a bearish hook reversal on the charts, a potential signal that futures are overbought and could correct lower. Notably, a similar hook reversal on 31 January saw a short-lived selloff, from which the market rallied to post its recent contract highs. Funds remain aggressive net buyers and rising open interest in corn futures further indicates a bullish outlook. Initial trendline support lies at $6.19 in the March contact ($6.19 ½ in May futures) and long-term trendline support at $6.04 ¼ below that ($6.05 in May futures).