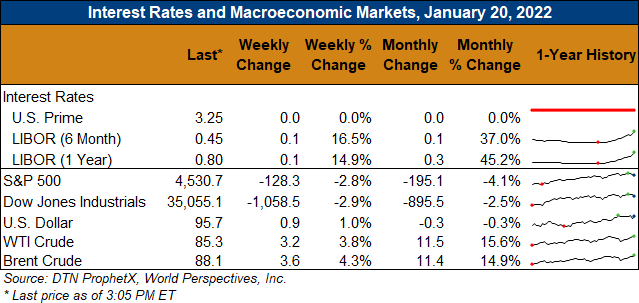

Outlook: March corn futures are 14 ¾ cents (2.5 percent) higher this week as funds added to their long position amid an increasingly bullish outlook. Grain markets are currently faced with three major bullish factors, two of which could have an immediate impact and another that will provide long-term support. The two more primary factors are the growing political tensions between Russia and Ukraine and the South American weather forecast. The long-term supporting factor is the U.S. inflation outlook and expectations that the Federal Reserve will raise interest rates in 2022.

World grain markets are moving higher in “risk-on” trade as Russia continues to amass troops along its border with Ukraine. World leaders’ calls for Russia to standdown have been unheeded so far and grain markets are preparing for the possibility of further escalations. Should Russia invade Ukraine, various world governments are likely to apply economic sanctions against the country, which would tighten exportable world grain supplies. Markets are moving higher ahead of any such action to ration non-Black Sea grain demand.

South American weather forecasts remains a threat

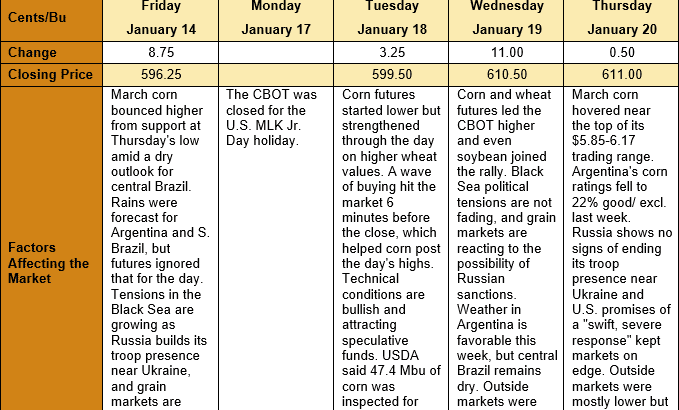

The South American weather forecasts remains a threat to 2022 world grain supplies. Recent precipitation across central Argentina, Uruguay, and parts of southern Brazil has been helpful for crops but will have limited impact regaining production lost so far. Due to the heat and drought, Argentina’s corn crop is now forecast at 48-50 MMT by private firms (the USDA’s January WASDE estimate is 54 MMT). Threats are also amassing for the Brazilian second-crop (safrinha) corn as the long-term weather outlook turns hot and dry for central and northern Brazil. While Brazilian farmers have planted just 2 percent of the safrinha crop so far, which means there is time for the weather forecast to change favorably. Markets, however, are already adding in a “weather premium” based on dry planting conditions and expectations for another dry safrinha growing season.

Speculative traders extended long positions

Funds and speculative traders have been expanding their long positions in CBOT markets amid a growing inflation outlook for the U.S. Economic inflation tends to support commodity prices. Investors often use commodities as a hedge against other inflationary impacts. The U.S. inflation rate reached 7.0 percent in December, the fastest pace in nearly 40 years, increasing expectations that the U.S. Federal Reserve will raise interest rates more quickly to curb inflation. Commodity exposure is appealing for investors and speculative traders during inflationary environments, helping support CBOT futures.

The weekly Export Sales report from USDA was delayed due to a U.S. holiday on Monday, but the Export Inspections report leaned bullish corn. Last week, the report showed corn inspections totalled 1.204 MMT, up 18 percent from the prior week. YTD inspections total 15.288 MMT, down 13 percent.

From a technical standpoint, March corn futures forged a trading range low at $5.85 ¼ on 13 January and made a bullish rally above $6.00 this week. Strong technical performance, combined with the bullish factors listed above, enticed traders back to the long side of the market. March corn is now targeting resistance at $6.17 ¾ (the 28 December daily high), forming the current trading range. Should the market trade be above that level, there is little technical resistance until the 10 June 2021 daily high at $6.33, followed by the contract high at $6.40.