The California Almond Board has released the Position report with March shipments of +281.07 million pounds of almonds compared to last year’s 244.98 million pounds for an increase of +14.7% percent. The 281 million pounds is a new record for March shipments. Exports lead the charge this month with an impressive 214 million pounds shipped in March. Unfortunately, Domestic was down -7.5% for the month, February has been the only positive month for domestic shipments.

Current shipments

| Million LBS | Percent | |

| Domestic | 66.44 | -7.5% |

| Export | 214 | +24% |

| COUNTRY | March MILLION LBS 2023 | March MILLION LBS 2022 |

| India | 27.0 | 23.0 |

| China | 24.7 | 6.5 |

| Spain | 21.0 | 29.6 |

| Germany | 15.0 | 11.8 |

| U.A.E. | 17.3 | 8.0 |

| Turkey | 9.7 | 5.2 |

YEAR-TO-DATE SHIPMENTS

+1.798 billion pounds compared to 1.683 billion pounds last year for an increase of +6.85 percent.

CROP RECEIPTS

Now at +2.540 billion pounds compared to last year’s 2.901 billion pounds for a decrease of 12.43 percent. The Objective Crop Estimate was at 2.6 billion pounds so we are very near to what the expectations were.

MARKET

Almond prices have continued to stay firm over the last few weeks, purchasing has been hand-to-mouth for prompt shipments. Growers are not certain about the damage to the new crop due to poor weather on bloom, and buyers are reluctant to cover at these levels until they have some confidence in the market.

As an industry, we were coming off an impressive Q1 shipment quarter. January, February and March were all record shipment months. Export markets are up 12.44% for Quarter 1 of 2022 for shipments. Domestically, we are behind last year’s Q1 shipments by -5.75%. New Sales for the month of the market were only at 143 million lbs. Due to lower sales, the carry-out will continue to increase with the possibility of reaching 800-850 million lbs. New crop sales have been few and far between, we expect this to continue until we can get a better feel for next year’s crop. For the current crop plus the carry-in, we are currently sold at 72.3%. Last year we were at 75%, so almost identical to last year.

Overall crop development on the new crops is approx. 7-10 days delayed due to the excessive rain and cooler temps over the past 2.5 months. In the next 4 weeks, we will start seeing more crop estimates from industry participants and also NASS, which will assist us to better gauge pricing in the market for the new and current crop.

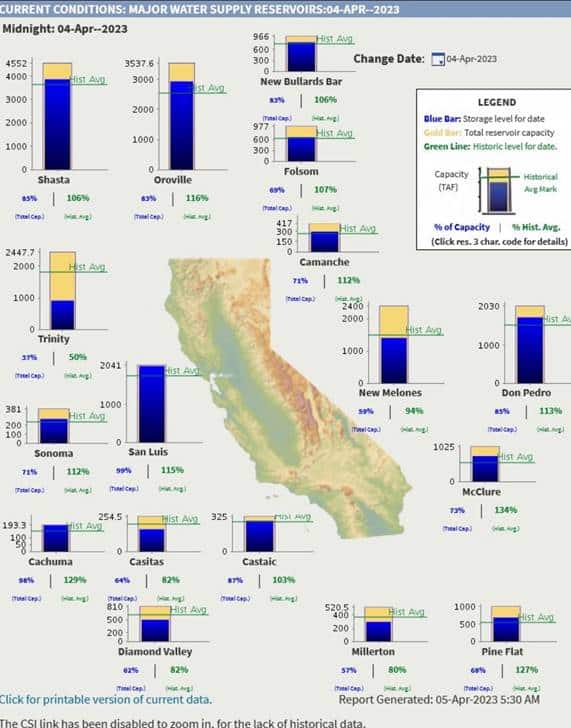

DROUGHT

Please see the below table for Major Water Supply Reservoirs in California. As you can see, California has had historic rain and snow throughout this winter. Most of our largest reservoirs ( Shasta, Oroville, San Pedro) etc. are above the historical storage level for the year. This is before we start seeing higher temperatures and snow melt from the mountain snow. This does not mean we are 100% out of drought, but it’s a big step in the right direction.

OUTLOOK APRIL

With the lack of sales over the last few weeks, we do expect April shipments to be weaker than shipments for April 2022.

Import/Export Statistics

Please click to reach our marketplace