OVERVIEW

May almond shipments were 196 million pounds and fell in the upper range of industry expectations. This is 1% lower compared to last month and 24% lower compared to last year’s record for the month of May. Exports, at 141 million pounds, were essentially flat versus last month but down 27% to last year. Domestic shipments were 55 million pounds, down 3% to last month and 14% to last year. Total year-to-date shipments are now flat to last year.

SHIPMENTS

India

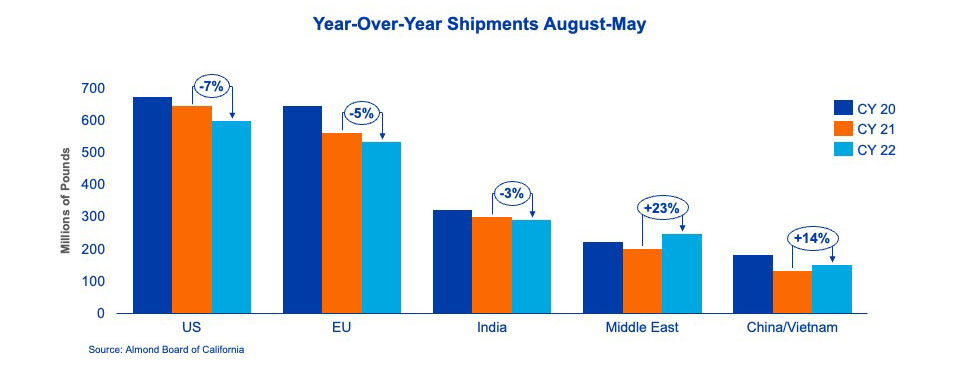

Shipments to this market were just under 20 million pounds for the month, down 42% to last May. The market is now down 3% for the crop year. Generally, the market remains uncovered for the balance of the crop season and with the new crop timing estimated to be two weeks later than last year, continued purchasing of the current crop will likely be needed to help support Diwali demand. This should help support California inshell price levels later in the season.

China

Shipments to China and Vietnam continued to ease and were 8.6 million pounds for the month, down 11%. Overall, this market is 14% ahead of last year’s pace. Given healthy destination inventories, this market has been very quiet in recent weeks with little purchasing being done from either California or Australia. Many believe the current stocks are sufficient to cover demand for the Mid-Autumn festival in late September.

Europe

As many expected, shipments to the European market were again softer than a year ago at 57 million pounds for the month, down 24% versus last May. This market is now down 5% for the season. As evidenced by the declining shipments, European demand is being funded by the previously built large inventory positions. There is no incentive to take excess coverage and replenish inventories in the short term with higher finance costs and better logistics. With Fall and 2023 holiday demand largely uncovered, it is likely that Europe will have stronger purchase intent in the next 6–8 weeks as we get closer to the objective estimate, likely setting stage for a more balanced quarterly shipment pattern in the 2023 crop season.

Middle East

As stated in previous reports, the Middle East has been a bright spot all season for California. Demand from the region from origin has slowed as they move through their heavier positions. The market remains up 23% year to date.

Domestic

The US market continues to see year-over-year declines with shipments now down 7% year to date. High food prices continue to impact consumer purchasing decisions and with recessionary pressures expected to continue into the next 12 months, consumer demand is likely to remain challenged.

COMMITMENTS

Commitments, at 483 million pounds, are down 21% compared to last year. Uncommitted inventory remains 2% higher versus last year at 677 million pounds. Market activity remained steady, albeit limited, last month with new sales at 114 million pounds. This is down 2% compared to last year. California is now 80% sold and shipped against total supply compared to 81% last year.

The May position report provides the first look at commitments for the 2023 crop year with total commitments reported at 57 million pounds. This is down 55% compared to last year and the lowest reported on record.

CROP

With the 2023 Subjective Estimate at 2.5 billion pounds behind us, the industry now eagerly awaits the Objective Estimate, which is tentatively scheduled to be released on July 7. The industry continues to review the developing crop with many observing a high degree of variability in quality from orchard to orchard. The crop is expected to yield less nonpareil given the unfavorable weather experienced during the bloom. Many anticipate the harvest to be later with crop development two weeks behind last season as a result of the uncharacteristic cooler weather experienced this spring in California.

Market PerspectiveAs expected, shipments continue to ease into the final months of the crop year. Despite the lower new crop projection, the market is reacting to the short-term inputs which is pressuring prices back to lower levels last seen prior to the almond bloom. This has done little to promote activity with buyers around the world who are largely covered for the balance of this crop year and continue to wait for more clarity before stepping in to purchase additional needs. California continues to search for opportunities to sell and ship the current crop and position itself for fall demand when many key markets will need to replenish inventories. The industry will continue to focus on the progression of the 2023 crop as well as the NASS Objective Estimate in July to provide more direction to the current market environment. |

Laura Gerhard

Vice President

To view Blue Diamond’s Market Updates and Bloom Reports Online Click Here

To view the entire detailed Position Report from the Almond Board of California Click Here