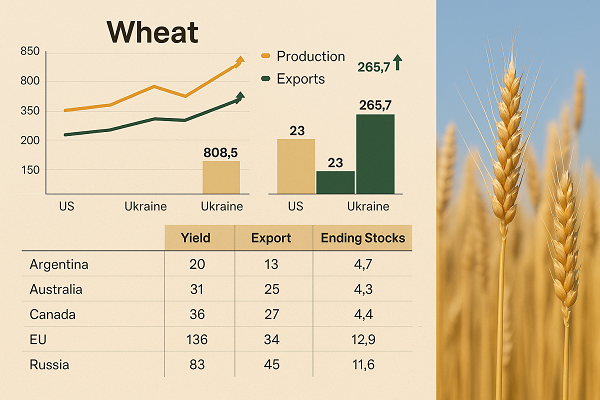

The global wheat market enters the 2025/26 marketing year with a distinctly bullish undertone, as USDA’s May report signals a robust rebound in worldwide production and exports. World wheat output is forecast to reach 808.5 million tons, up 8.81 million tons from last season, while exports are set to climb to 213 million tons. This expansion is driven primarily by the European Union, Russia, and Canada, with the EU’s output alone surging by 13.8 million tons. However, this optimism is tempered by regional challenges, notably a reduction in the US and Ukrainian harvests. The US crop is projected at 52.28 million tons, down 1.37 million tons year-on-year, while Ukraine faces a slight decline to 23 million tons. Despite these pockets of contraction, global ending stocks are forecast to edge higher to 265.7 million tons, reflecting ample supply and potentially capping upward price momentum in the near term. Weather volatility, particularly in the Black Sea and North American regions, remains a crucial watchpoint for yield realization. For market participants, the interplay between growing global surpluses and regional supply risks will define trading strategies in the weeks ahead.

Exclusive Offers on CMBroker

Wheat

protein min. 9,50%

98%

FCA 0.23 €/kg

(from UA)

Wheat

protein min. 11.50%

98%

FCA 0.25 €/kg

(from UA)

Wheat

protein min. 11.50%

98%

FCA 0.24 €/kg

(from UA)

📈 Prices

| Exchange/Location | Type | Protein | Delivery | Latest Price (USD/kg) | Weekly Change | Sentiment |

|---|---|---|---|---|---|---|

| Kyiv (UA) | Wheat | min. 9.50% | FCA | 0.23 | 0.00 | Neutral |

| Odesa (UA) | Wheat | min. 9.50% | FCA | 0.25 | 0.00 | Neutral |

| Kyiv (UA) | Wheat | min. 11.50% | FCA | 0.24 | 0.00 | Neutral |

| Odesa (UA) | Wheat | min. 11.50% | FCA | 0.26 | 0.00 | Neutral |

| Odesa (UA) | Wheat | min. 12.50% | FOB | 0.21 | 0.00 | Neutral |

| Odesa (UA) | Wheat | min. 11.00% | FOB | 0.20 | 0.00 | Neutral |

| Odesa (UA) | Wheat | min. 10.50% | FOB | 0.20 | 0.00 | Neutral |

| CBOT (US) | Wheat | min. 11.50% | FOB | 0.22 | 0.00 | Neutral |

| Paris (FR) | Wheat | min. 11.00% | FOB | 0.26 | 0.00 | Neutral |

🌍 Supply & Demand

- World production: 808.5 mln t (+8.81 mln t YoY)

- World exports: 213 mln t (+6.87 mln t YoY)

- World ending stocks: 265.7 mln t (+0.52 mln t YoY)

- US production: 52.28 mln t (-1.37 mln t YoY)

- Ukraine production: 23 mln t (-0.4 mln t YoY)

- EU production: 136 mln t (+13.8 mln t YoY)

- Russia production: 83 mln t (+1.4 mln t YoY)

- China production: 142 mln t (+1.9 mln t YoY); imports 6 mln t (+2.7 mln t)

📊 Fundamentals

| Country | Production (mln t) | Export (mln t) | Ending Stocks (mln t) |

|---|---|---|---|

| Argentina | 20 (+1.46) | 13 (+2) | 4.65 (-0.29) |

| Australia | 31 (-3.11) | 25 (-2) | 4.32 (+0.1) |

| Canada | 36 (+1.04) | 27 (0) | 4.39 (+0.3) |

| EU | 136 (+13.8) | 34 (+7.5) | 12.86 (+0.5) |

| Russia | 83 (+1.4) | 45 (+1.5) | 11.59 (-0.2) |

| Ukraine | 23 (-0.4) | 16.5 (+0.5) | 1.49 (0.0) |

| US | 52.28 (-1.37) | 21.77 (-0.55) | 25.12 (+2.22) |

| China | 142 (+1.9) | 6 (imports) (+2.7) | 123.9 (-3) |

🌦️ Weather Outlook

- Black Sea Region: Mild spring has supported crop development, but pockets of dryness in southern Russia and eastern Ukraine could limit yield potential if dry conditions persist through May.

- US Plains: Mixed conditions—northern Plains see adequate moisture, while southern Plains remain drier than average, raising concerns for hard red winter wheat.

- EU: Western Europe has benefited from above-average rainfall, improving soil moisture profiles and supporting the region’s production surge.

- Australia: Early planting in eastern states has seen some rainfall deficits, but forecasts suggest a return to normal precipitation by late May.

🔎 Market Drivers

- USDA May report: Upward revision in global output and exports, but US and Ukraine face production headwinds.

- Speculative positioning: Funds remain net short on CBOT wheat, but short covering could trigger price volatility if weather risks materialize.

- Global inventories: Stocks remain ample, especially in China and the EU, tempering price rallies.

- Geopolitical risk: Ongoing Black Sea tensions continue to pose a supply risk premium for Ukrainian and Russian exports.

📆 Trading Outlook & Recommendations

- Expect range-bound trading in the short term as global supplies improve, but monitor weather in key regions for potential upside risk.

- End users should consider locking in forward contracts for Q3-Q4 2025 to hedge against weather-driven volatility.

- Exporters in the EU and Russia may benefit from competitive pricing and robust demand from Asia and North Africa.

- Speculators: Watch for potential short-covering rallies if dryness intensifies in the Black Sea or US Plains.

🔮 3-Day Regional Price Forecast

| Exchange/Location | Current Price (USD/kg) | Forecast (USD/kg) | Direction |

|---|---|---|---|

| CBOT (US) | 0.22 | 0.22 – 0.23 | Stable to Slightly Up |

| Paris (FR) | 0.26 | 0.26 – 0.27 | Stable |

| Kyiv (UA) | 0.23 – 0.24 | 0.23 – 0.24 | Stable |

| Odesa (UA) | 0.20 – 0.26 | 0.20 – 0.26 | Stable |