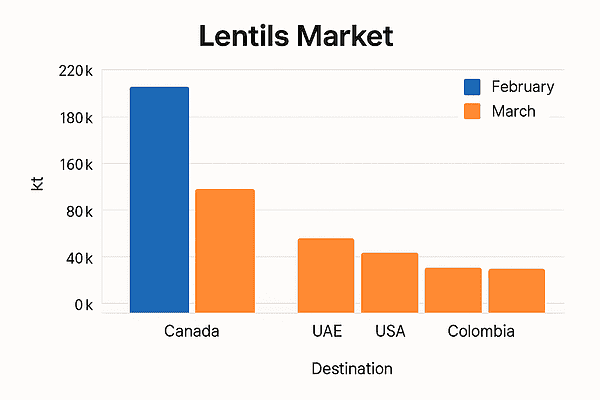

The global lentils market is experiencing significant shifts in trade flows and demand dynamics as we move through May 2025. Canadian lentil exports, a key barometer for global supply, have seen a sharp downturn in March compared to February, primarily due to a notable drop in Indian demand. India, traditionally the largest importer of Canadian lentils, has slipped out of the top three buyer countries this season. This is attributed to improved domestic supply in India and persistently soft prices, reducing the incentive for importers to source from Canada. As a result, Canadian lentil exports plummeted from 218,978 tonnes in February to just 81,226 tonnes in March. The United Arab Emirates, the US, and Colombia have emerged as the leading alternative destinations for Canadian lentils in March. Despite these short-term disruptions, cumulative Canadian lentil exports for the first eight months of the marketing season are up significantly year-on-year, highlighting the market’s resilience and the shifting landscape of global demand. Meanwhile, prices for key lentil varieties remain steady, reflecting a balance between ample supply and subdued international buying interest. Weather conditions in major growing regions and the evolving trade policies in India—especially concerning duty-free imports—remain crucial factors for the market outlook in the coming months.

Exclusive Offers on CMBroker

Lentils dried

small, green

99.5%

FOB 1.23 €/kg

(from CN)

Lentils dried

small, green

99.5%

FOB 1.15 €/kg

(from CN)

Lentils dried

Red football

FOB 2.60 €/kg

(from CA)

📈 Prices

| Product | Type | Origin | Location | Purity | Organic | Delivery Terms | Latest Price (USD/kg) | Previous Price (USD/kg) | Update Date | Market Sentiment |

|---|---|---|---|---|---|---|---|---|---|---|

| Lentils dried | Small, Green | CN | Beijing | 99.5% | Yes | FOB | 1.43 | 1.44 | 2025-05-14 | Stable/Soft |

| Lentils dried | Small, Green | CN | Beijing | 99.5% | No | FOB | 1.30 | 1.31 | 2025-05-14 | Stable/Soft |

| Lentils dried | Red Football | CA | Ottawa | – | No | FOB | 2.47 | 2.47 | 2025-05-08 | Stable |

| Lentils dried | Laird, Green | CA | Ottawa | – | No | FOB | 1.63 | 1.63 | 2025-05-08 | Stable |

| Lentils dried | Eston Green | CA | Ottawa | – | No | FOB | 1.50 | 1.50 | 2025-05-08 | Stable |

🌍 Supply & Demand

- Canadian Lentil Exports: Fell sharply in March 2025 (81,226 tonnes) vs. February (218,978 tonnes), mainly due to weak Indian demand.

- India’s Role: India, typically the top buyer, dropped out of the top three importers in March due to better domestic supply and soft prices.

- Alternative Buyers: UAE (16,089 tonnes), USA (10,634 tonnes), and Colombia (10,634 tonnes) became the main importers from Canada in March.

- Cumulative Season Exports: Canadian lentil exports for the first 8 months of the 2024/25 season reached 1,520,958 tonnes (up from 1,193,393 tonnes in 2023/24).

- Peas & Kabuli Gram: Pea exports also declined, and Kabuli gram exports rose, but India remains absent as a significant buyer.

📊 Fundamentals

- Global Inventories: Higher carryover stocks in India and improved local harvests are dampening import needs.

- Speculative Positioning: Traders remain cautious, with limited forward buying due to uncertain Indian import policy and softening prices.

- Trade Policy: Duty-free import of yellow peas continues in India, but with little impact on Canadian shipments.

⛅ Weather Outlook

- Canada: Weather has been broadly favorable for seeding and early crop development in the Prairies, supporting potential for a good harvest if conditions persist.

- India: Monsoon outlook is positive, likely supporting another strong pulse harvest and further reducing import requirements.

- Other Regions: No major adverse weather events reported in other key lentil producing/exporting countries.

🌐 Global Production & Stocks

| Country | 2024/25 Production Estimate (tonnes) | 2024/25 Export Estimate (tonnes) | Stock Situation |

|---|---|---|---|

| Canada | ~2,500,000 | 1,520,958 (to Mar) | Comfortable, but declining exports |

| India | ~1,300,000 | Minor | High, due to good harvests |

| Australia | ~500,000 | Major exporter | Stable |

| Turkey | ~350,000 | Minor exporter | Stable |

📆 Trading Outlook & Recommendations

- Monitor Indian import policy closely—any change could rapidly shift export demand and prices.

- Expect continued soft-to-stable prices in the short term due to ample supplies and weak Indian demand.

- Watch Canadian weather for signs of stress—any adverse development could support new-crop prices.

- Consider forward contracting only on price dips or if Indian demand signals improve.

- Importers: Diversify sourcing beyond Canada, especially as Indian and UAE buying patterns shift.

🔮 3-Day Regional Price Forecast

| Location | Product/Type | Current Price (USD/kg) | 3-Day Forecast (USD/kg) | Trend |

|---|---|---|---|---|

| Beijing, CN | Small Green (Organic) | 1.43 | 1.42 – 1.44 | Stable |

| Beijing, CN | Small Green (Conventional) | 1.30 | 1.29 – 1.31 | Stable |

| Ottawa, CA | Red Football | 2.47 | 2.47 | Stable |

| Ottawa, CA | Laird Green | 1.63 | 1.62 – 1.64 | Stable |

| Ottawa, CA | Eston Green | 1.50 | 1.50 | Stable |