The global rapeseed market is entering a period of heightened volatility and uncertainty as we move into the 2025/26 marketing year. While USDA forecasts suggest a moderate recovery in global rapeseed production—up 5.2% to 89.56 million tons—persistent weather challenges and regional disparities are likely to keep markets on edge. Notably, the European Union is expected to see a modest rebound, but production will still fall short of 2023/24 levels. Canada and India are also projected to increase output, but Australia’s gains remain marginal. The most dramatic shift is unfolding in Ukraine, where a combination of drought, frost, and re-sowing has slashed the harvest outlook from the USDA’s 3.7 million tons to local estimates of just 2-2.5 million tons. This sharp reduction is already fueling a rally in forward prices, with Black Sea port offers climbing $10-15/t in a week. Meanwhile, Paris rapeseed futures have surged, supported by tightening Ukrainian supply and robust EU demand, despite a forecasted 21% drop in EU imports next season. Canola prices in Canada have also reached seasonal highs, but remain sensitive to global oil trends and trade policy uncertainties. As weather risks persist, particularly in Ukraine and Canada, and with speculative buying intensifying, rapeseed prices are poised for further volatility in the months ahead.

Exclusive Offers on CMBroker

Rape seeds

42% min oil

98%

FCA 0.61 €/kg

(from UA)

Rape seeds

42% min oil

98%

FCA 0.62 €/kg

(from UA)

Rape seeds

FOB 0.57 €/kg

(from FR)

📈 Prices

| Exchange/Origin | Product | Location | Closing Price | Weekly Change | Market Sentiment |

|---|---|---|---|---|---|

| Paris (Euronext) | Rapeseed Futures (Aug 2025) | France | €484/t ($542/t) | +3.2% | Bullish |

| ICE (Winnipeg) | Canola Futures (Jul 2025) | Canada | 730 CAD/t ($522/t) recent: 705 CAD/t |

High, then -3.4% | Volatile |

| Black Sea (Forward) | Rapeseed (Jul Delivery) | Ukraine | $515–525/t | +2.0–3.0% | Bullish |

| Physical (Kyiv) | Rape seeds, 42% min oil | Ukraine | $0.51/kg | Stable | Neutral |

| Physical (Paris) | Rape seeds | France | $0.54/kg | Stable | Neutral |

🌍 Supply & Demand

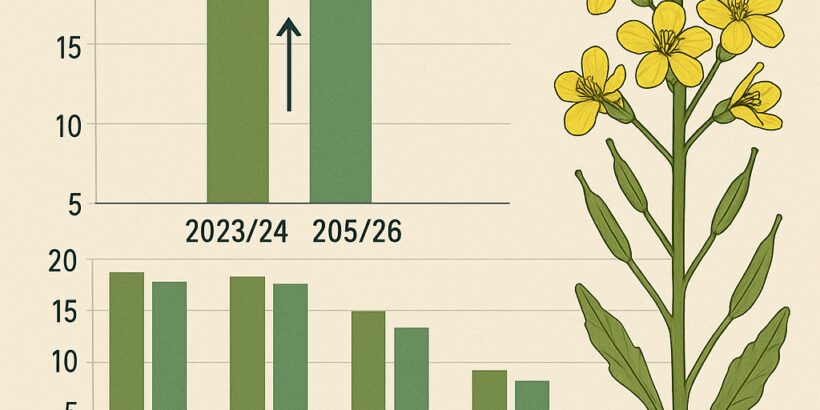

- Global Production (2025/26 MY): 89.56 mln t (+5.2% y/y), nearly matching 2023/24’s 89.9 mln t.

- EU Output: 19.15 mln t (down from 20.45 mln t in 2023/24).

- Canada: 19.5 mln t (up 0.7 mln t y/y).

- India: 12 mln t (up 0.5 mln t y/y).

- Russia: 5.3 mln t (up 0.65 mln t y/y).

- Australia: 6.15 mln t (up 0.21 mln t y/y).

- Ukraine: USDA: 3.7 mln t; Local estimate: 2–2.5 mln t due to weather losses and reduced area.

- EU Imports: Forecast to fall 21% to 5.8 mln t, with Ukraine still the top non-GMO supplier.

📊 Fundamentals

- USDA Reports: Projected global recovery, but Ukrainian output likely overestimated.

- Speculative Positioning: Traders ramp up forward purchases in Ukraine, driving up prices.

- Inventories: Tightening stocks in Ukraine and the EU support prices; Canadian stocks steady.

- Import Flows: Ukraine supplied 2.36 mln t to EU by early May (41.5% of EU imports, down from 3 mln t last year).

🌦️ Weather Outlook

- Ukraine: Persistent dryness in August-September 2024 reduced sowing area. Frosts in March-April 2025 caused significant crop losses and forced re-sowing. Weather remains a key risk for final yields.

- Canada: Variable spring moisture; some regions face dryness, but high prices may boost sowings. Weather in June-July will be critical for yield potential.

- EU: Generally favorable spring weather, though some localized dryness reported in Germany and Eastern Europe.

🌐 Global Production & Stock Comparison

| Country | 2023/24 Output (mln t) | 2024/25 Output (mln t) | 2025/26 Forecast (mln t) | Stocks Trend |

|---|---|---|---|---|

| EU | 20.45 | 16.86* | 19.15 | Lower |

| Canada | 19.2 | 18.8* | 19.5 | Stable |

| India | 11.52 | 11.7* | 12 | Stable |

| Russia | 4.2 | 4.65* | 5.3 | Higher |

| Australia | 6.05 | 5.7* | 6.15 | Stable |

| Ukraine | 4.75 | 3.7* | 2–2.5 (local est.) | Significantly lower |

*Estimated based on local and USDA data

📆 Trading Outlook & Recommendations

- Short-term bullish momentum likely to continue due to Ukrainian supply risks and strong speculative buying.

- Monitor weather developments in Ukraine and Canada closely—any further adverse events could trigger price spikes.

- EU crushers should consider forward coverage; import flows from Ukraine may remain constrained.

- Canadian farmers are incentivized to increase canola plantings, but global oil prices and trade policy remain key risks.

- Physical buyers in the EU and Asia should watch for price pullbacks to secure supply for Q3–Q4 2025.

🔮 3-Day Regional Price Forecast

| Market | Current Price | 3-Day Forecast | Trend |

|---|---|---|---|

| Paris (Euronext Aug) | €484/t ($542/t) | €485–490/t ($543–550/t) | ⬆️ Slightly higher |

| Black Sea (UA fwd) | $515–525/t | $520–530/t | ⬆️ Firm |

| ICE Canola (Jul) | 705 CAD/t ($504/t) | 700–715 CAD/t ($500–510/t) | ⬆️/⬇️ Volatile |