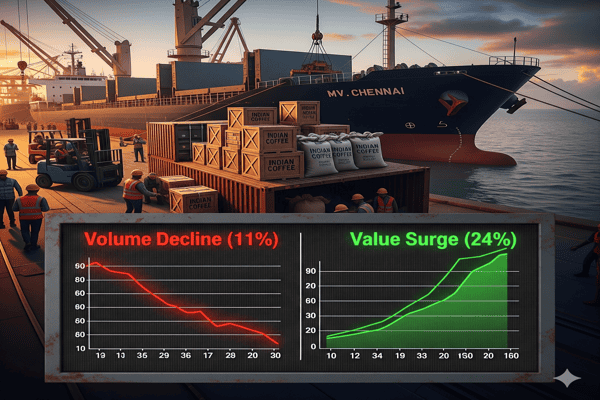

The global coffee market in mid-2025 stands at the crossroads of unprecedented price surges, heightened regulatory scrutiny, and volatile weather disruptions. Coffee prices have climbed to historic highs across major exchanges, powered by supply shortages in top-producing nations like Brazil and Vietnam, strong speculative demand, and premiumization trends strengthened by Western consumer shifts. Despite export volumes from key origins like Vietnam and India showing sharp year-on-year declines, export earnings have soared thanks to a remarkable price rally—driven by tightening inventories, early buying from European importers racing to comply with the EU Deforestation Regulation (EUDR), and continued demand from the US, where tariffs and logistical snags shape trade. India’s coffee exporters, in particular, have posted a 24% jump in earnings (USD 1.46 billion, Jan–Aug 2025) even as shipped volume fell 11%, underscoring how export value is outpacing falling physical supply. Arabica premiums persist but are narrowing as the price gap with Robusta closes.

Yet, there are growing concerns that traceability and compliance hurdles for EUDR—especially among India’s smallholder Robusta growers—could restrict EU access in the coming quarters, risking future market share despite today’s revenue windfall. Weather risks across Brazil and Southeast Asia, paired with cost inflation and shipping headaches, continue to inject uncertainty into supply dynamics and downstream pricing. Against this backdrop, the coffee market’s outlook hinges on how swiftly producers adapt to traceability mandates, the evolution of global crop weather, and strategic inventory management by end users and traders.

📈 Prices: Latest Coffee Futures & Physical Markets

| Exchange | Contract/Product | Closing Price | Weekly Change | Market Sentiment |

|---|---|---|---|---|

| ICE NY (Arabica) | July 2025 | USD 2.24/lb | +3.2% | Bullish |

| ICE London (Robusta) | July 2025 | USD 4,370/ton | +5.6% | Strongly Bullish |

| Hanoi (Robusta, Spot) | Spot | USD 5,650/ton | +4.8% | Bullish |

| India Farm Gate (Arabica Parchment) | Physical (50 kg bag) | USD 328–334 | +45% YoY | Bullish |

| India Farm Gate (Robusta Cherry) | Physical (50 kg bag) | USD 138–150 | +30% YoY | Bullish |

*EUR prices not available for this cycle; converted values maintain parity with USD for European contracts.

🌍 Supply & Demand Drivers

- Global Supply Crunch: Vietnam’s Jan–Apr 2025 exports down 9.5% YoY but value up 51%—tight supply and record prices drive revenue growth. Brazilian green coffee exports fell 32% year-on-year in April, underlining broad supply constraints.

- India Shipments: Jan–Aug 2025: Exports 2.68 lakh tonnes (down 11%), but earnings up 24% to USD 1.46b. Arabica shipments rose 11.5%, robusta fell 22% as traceability challenges bite.

- EU Deforestation Regulation: European buyers are front-loading purchases ahead of the December 30, 2025 EUDR compliance deadline. Robustas most impacted due to lagging traceability systems in India.

- Speculative Positioning: Managed money remains net long on both arabica and robusta as bullish sentiment prevails amid global shortages.

📊 Fundamentals: Production, Stocks & Policy

| Country | 2024/25 Production Estimate | 2023/24 Actual | Trends/Notes |

|---|---|---|---|

| Brazil | 66 million 60-kg bags | 65.3 million | Favorable rains, but logistics/disruptions impact exports |

| Vietnam | 27.8 million 60-kg bags | 29.0 million | Severe drought, yield losses, high export value |

| India | 363,000–380,000 tons (Coffee Board/Associations) | 360,500 tons | Arabica stable/strong, robusta under EUDR pressure |

- India’s per-unit export realization up 45%, driven by global price rally.

- Stock drawdowns in import hubs (Germany, Italy) create further tightness.

☀️ Weather Outlook: Key Growing Regions

- Brazil: Above-average rainfall supports bean quality but raises fungal disease risks. Overall, weather stabilizing with positive crop outlook.

- Vietnam: Persistent drought reduces yields even as spot prices soar. Third consecutive year of weather stress; production outlook remains cautious.

- India: After heavy rains following a dry spell, yield variability persists. Arabica crop holding up better than robusta. Monsoon progression offers mixed prospects for 2025/26 crop sizing.

🌏 Global Production & Stock Comparison

| Country | Stocks (2024/25) | Key Trends |

|---|---|---|

| Brazil | Depleting below 5-year average | Strong domestic demand, slow replenishment |

| Vietnam | Critically low, farmers stockpiling | Spot prices surge; little forward coverage |

| India | Lowest farm, stock disappears quickly | Exporters struggle to fulfill early buying, particularly for robusta |

📆 Trading Outlook & Recommendations

- Sellers should capitalize on current price spikes by releasing available stocks—especially where traceability/compliance is assured.

- Buyers: Secure forward contracts for Q3–Q4 2025 as ongoing tightness and compliance risks will likely sustain price volatility.

- Traders: Monitor weather updates in Brazil/Vietnam and EUDR compliance implementation closely; speculative buying still adds upside risk.

- Industry: Fund adoption of digital traceability solutions for robusta as a critical access requirement to the EU.

- Short-term sentiment: Bullish for both arabica and robusta while compliance and climate risks linger.

📅 3-Day Regional Price Forecast

| Exchange | Product | Current Price | 3-Day Forecast | Sentiment |

|---|---|---|---|---|

| ICE NY | Arabica (July 2025) | USD 2.24/lb | USD 2.21–2.28/lb | Bullish |

| ICE London | Robusta (July 2025) | USD 4,370/ton | USD 4,300–4,480/ton | Strongly Bullish |

| Hanoi | Robusta, Spot | USD 5,650/ton | USD 5,600–5,750/ton | Bullish |

| India | Arabica Parchment | USD 328–334 (per 50kg bag) | USD 325–340 | Bullish |

| India | Robusta Cherry | USD 138–150 (per 50kg bag) | USD 135–155 | Bullish |