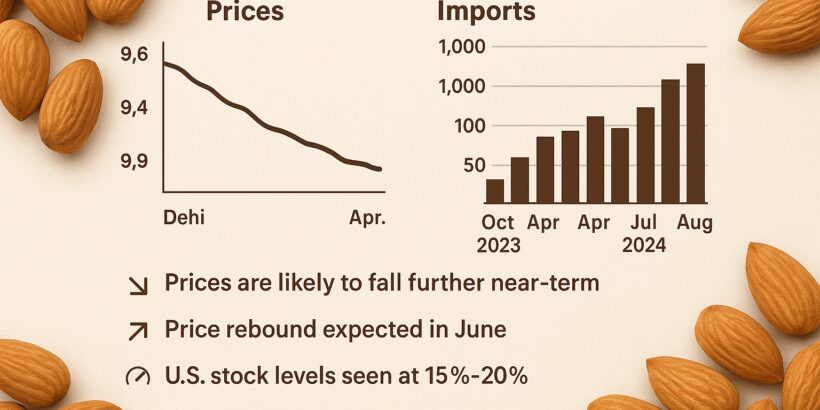

The global almonds market is currently experiencing a period of price softness, driven by a surge in import volumes and seasonally weaker demand. In India, one of the world’s largest almond importers, prices have declined by $0.12–$0.18 per kilogram in Delhi, now ranging between $9.41 and $9.46/kg. This downward trend is largely attributed to record import volumes in April 2025, which saw 1,454 containers arriving—just shy of the October 2023 peak. Consistent high-volume imports throughout 2024 have kept domestic stocks robust, further reducing any immediate upward price pressure.

The market’s current sentiment is shaped by both supply-side abundance and demand-side seasonality. As summer sets in, almond consumption typically drops, extending the price softness. Despite this, there are early signs of a cautious bullish outlook emerging. U.S. almond stocks are reportedly at 15–20% of capacity, with the new crop not expected until August. This tightening supply, coupled with global inventory drawdowns, could set the stage for a price rebound as early as June. American almond prices, meanwhile, are quoted at $2.50–$2.55/lb, reflecting stable but watchful market conditions. Traders and importers are closely monitoring U.S. stock levels and weather patterns in California, the world’s leading almond producer, for any signs of supply disruptions. In summary, while short-term prices are expected to remain under pressure, tightening stocks and seasonal shifts could trigger a reversal in the coming weeks.

Exclusive Offers on CMBroker

Almonds kernels

carmel, ssr, 18/20

FAS 6.70 €/kg

(from US)

Almonds kernels

carmel, ssr 20/22

FAS 6.65 €/kg

(from US)

Almond kernels

marcona, 12/14

FOB 6.60 €/kg

(from ES)

📈 Prices

| Product | Origin | Type | Location | Delivery Terms | Latest Price (USD/kg) | Previous Price (USD/kg) | Weekly Change | Market Sentiment |

|---|---|---|---|---|---|---|---|---|

| Almonds kernels | US | Carmel, SSR, 18/20 | Washington D.C. | FAS | 6.90 | 6.87 | +0.03 | Soft/Bearish |

| Almonds kernels | US | Carmel, SSR 20/22 | Washington D.C. | FAS | 6.85 | 6.82 | +0.03 | Soft/Bearish |

| Almond kernels | ES | Marcona, 12/14 | Madrid | FOB | 6.80 | 6.77 | +0.03 | Stable |

| Almond kernels | ES | Marcona, 14/16 | Madrid | FOB | 8.40 | 8.37 | +0.03 | Stable |

| Almonds kernels (organic) | US | Natural, 27/30, Nonpareil SSR | Washington D.C. | FOB | 9.50 | 9.47 | +0.03 | Stable |

| Almond kernels | ES | Marcona, S/16 | Madrid | FOB | 9.10 | 9.07 | +0.03 | Stable |

| Almond kernels | ES | Valencia, 10/12 | Madrid | FOB | 5.75 | 5.72 | +0.03 | Stable |

| Almond kernels | ES | Valencia, 12/14 | Madrid | FOB | 5.75 | 5.73 | +0.02 | Stable |

| Almond kernels | ES | Valencia + 14 mm | Madrid | FOB | 6.16 | 6.16 | 0.00 | Stable |

| Almond kernels | ES | Guara bajo, 12 | Madrid | FOB | 5.80 | 5.77 | +0.03 | Stable |

| Almond kernels | ES | Guara, 12/14 MMS | Madrid | FOB | 6.10 | 6.07 | +0.03 | Stable |

| Almond kernels | ES | Guara, S/14 | Madrid | FOB | 6.30 | 6.27 | +0.03 | Stable |

| Almonds, inshell | IR | Sangi | Tehran | FOB | 1.75 | 1.64 | +0.11 | Firm/Bullish |

| Almond kernels | IR | Mamra, grade a | Tehran | FOB | 11.17 | 10.45 | +0.72 | Firm/Bullish |

🌍 Supply & Demand

- Imports: April 2025 saw 1,454 containers imported to India, the highest since October 2023 (1,523 containers). High import volumes in January, April, May, September, and December 2024 have kept domestic stocks ample.

- Consumption: Summer months typically see reduced almond consumption in key markets, further softening prices.

- Stocks: U.S. almond inventories are estimated at 15–20% of capacity, with nearly three months of demand still to be met before the new crop arrives in August.

- Global Quotes: American almonds are quoted at $2.50–$2.55/lb, indicating stable but watchful conditions.

📊 Fundamentals

- Recent Drivers: High import volumes, strong stocks, and seasonal demand weakness are the main drivers of current price softness.

- USDA Reports: Market participants are closely watching for updates on U.S. crop progress and stock levels as the season advances.

- Speculative Positioning: Short-term sentiment remains bearish due to ample supply, but tightening U.S. stocks are supporting a cautiously bullish medium-term outlook.

🌦️ Weather Outlook

- California: Weather in California, the world’s largest almond producing region, is currently stable with no major adverse events reported. Mild temperatures and sufficient irrigation are supporting crop development. However, any heatwaves or unexpected storms could impact yield projections as the crop approaches maturity in June–July.

- Spain: Spanish almond regions are experiencing typical spring conditions, with adequate rainfall supporting healthy bloom and nut set.

🌐 Global Production & Stocks

| Country | 2024/25 Production Estimate (kt) | 2024/25 Ending Stocks (kt) | Notes |

|---|---|---|---|

| USA | 1,250 | 180 | Stocks tightening, new crop in August |

| Spain | 105 | 35 | Healthy crop, stable stocks |

| Iran | 120 | 20 | Firm export demand |

| India (Import) | N/A | Estimated 3 months supply | High recent imports |

📆 Trading Outlook & Recommendations

- Short-term (next 2–3 weeks): Prices are expected to remain under pressure due to high stocks and subdued demand.

- Medium-term (June onward): Watch for potential rebound as U.S. stocks tighten and new crop uncertainty increases.

- Buyers: Consider staggered purchases, taking advantage of current softness, but monitor U.S. stock reports closely.

- Sellers: Hold off on large sales if possible; improved pricing may emerge as inventories draw down in late June–July.

- Speculators: Short-term bearish, but position for a possible pre-harvest rally in late June or July.

🔮 3-Day Regional Price Forecast

| Region/Exchange | Current Price (USD/kg) | Forecast (Next 3 Days) | Trend |

|---|---|---|---|

| Delhi (Spot) | 9.41–9.46 | 9.35–9.45 | Soft/Lower |

| US (FAS, Washington D.C.) | 6.85–6.90 | 6.80–6.90 | Stable/Soft |

| Spain (FOB, Madrid) | 5.75–8.40 | 5.70–8.35 | Stable |