OVERVIEW

Shipments of blue diamond almonds for the month of March exceeded market expectations while setting a record for the third consecutive month as the industry topped with 281 million pounds. This is 14.4% higher than last month and 14.7% higher than last year. Export shipments continue to gain momentum having now improved month over month for four consecutive months. This is the strongest export performance of the year at 215 million pounds which is up 14.0% to last month and 24.0% to last year. The Domestic market also saw month-over-month growth with 66.4 million pounds of shipments, up 15.6% from last month, but down 7.5% from last year. This now puts total shipments at 1.8 billion pounds, ahead of last year by 6.8%.

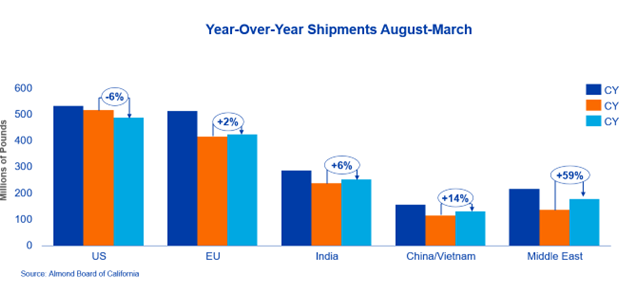

SHIPMENTS

India

Shipments to India were 27.5 million pounds for the month, down 19.6% from last month and up 15.0% from last year. India has shipped a consistent 32 to 35 million lbs for the prior 6 months. With pricing for inshell firming over the course of the last 6 weeks, we have seen the market pull back on purchases resulting in a lower shipment number for the month. The market still has demand to cover for the May/June shipment period and is expected to come back in the coming weeks to cover their future demand.

China

Shipments were strong for a second consecutive month at 24.7 million pounds. This is up 13% from last month and 275% from last year. YTD shipments to China now outpace last year by 19% after having trailed for the first half of the crop year. Buying activity has gone quiet after 3 months of active purchasing to restock supplies following the removal of COVID restrictions. This has resulted in local market prices being lower than California offers further muting demand. Australia is now offering to China although the limited business has been done given weak nearby demand. The market is expected to remain calm as it enters the quiet period of the late spring and summer months.

Europe

Shipments to the European market were down 8% for the month compared to last year. Processors and traders throughout the region took long positions in January at the lower levels. Overall, European demand is subdued given continuing macroeconomic challenges throughout the region. Purchasing in Europe has backed off over the last month as pricing firmed. Europe will likely continue to be challenged to reach last year’s robust shipment numbers for the upcoming months.

Middle East

Shipments to the Middle East continue at an exceptional pace with the market now up 59% year to date and March up 90% to last year. The Middle East has continued to be a strong driver of global consumption this season as low market prices have driven exceptional volume year-to-date.

Domestic

Domestic shipments were recorded at 66.4 million pounds, a 7.5% decline versus last year. Key channels and categories driving almond consumption continue to face headwinds with inflationary pressures affecting consumer spending habits. Expectations are for current demand patterns to persist for the balance of the crop year.

COMMITMENTS

March commitments now sit at 647 million pounds which is down 22% to last year. New sales for the month were disappointing at 143 million pounds, down 35% to last year. This can be attributed to reduced activity from buyers and sellers alike given the uncertainty of new crop production resulting from the unfavorable bloom weather in February and into March. Uncommitted inventory is now 881 million pounds, down 5.9% to last year. Sold and shipped as a percent of the total supply (assuming a 2.55 billion pound crop) is 73.3% compared to 72.5% last year.

CROP

Many in the market are anxious to understand the effects of the unfavorable bloom weather on the 2023 almond crop. We are still weeks away from understanding the impact on production and ultimately its effect on price. The industry will continue to monitor the progress of the crop while various estimates will be released in the coming weeks offering some additional forecast and perspective, inclusive of the NASS Subjective estimate on May 12.

Market PerspectiveShipments continued their strong pace in March turning in another season high and third consecutive month of record shipments over the prior year. Strong sales activity in December and January pushed shipments in both February and March, allowing the industry to maintain momentum to date. Export shipments continue to lead the way and are now ahead of last year’s pace. Domestic shipments continue to lag. Leading up to the almond bloom, prices had been relatively stable. Price has firmed in recent weeks given the poor bloom weather received in February and March. This has dampened buying and selling activity in the short term as evidenced by the low new sales figure reported for the month. Favorable uncommitted inventories and strong shipments to date have set the industry up well to draw down the carryout to more manageable levels. The industry focus is on closing out the balance of this crop year as the market awaits news on the 2023 crop. As California turns to warmer and drier weather, the market continues to monitor the progression of the 2023 crop. It will take weeks to understand the impact of the unfavorable bloom weather and what it means to almond production. The industry’s first official estimate (NASS Subjective Estimate) will release on May 12 and attempt to offer a glimpse of what to expect for the upcoming new crop. |

Laura Gerhard

Vice President

To view Blue Diamond’s Market Updates and Bloom Reports Online Click Here

To view the entire detailed Position Report from the Almond Board of California Click Here