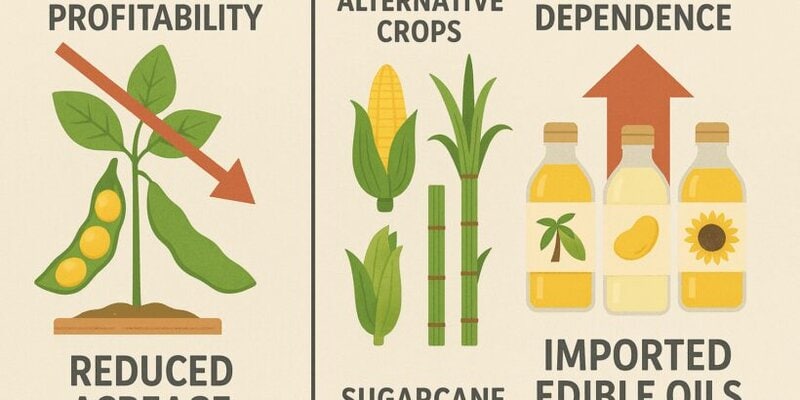

The global soybean market is entering a period of notable volatility, with India—one of the world’s key soybean producers and the largest importer of edible oils—at the center of a significant shift. Farmers across India’s major soybean-growing states are increasingly abandoning the crop in favor of alternatives like corn and sugarcane, lured by higher profitability and more stable returns. This trend is expected to sharply reduce India’s domestic soybean output for the 2025 season, leading to a greater reliance on imports of edible oils such as palm, soya, and sunflower oil. The Soybean Processors Association of India (SOPA) reports that local soybean prices have persistently trailed the government’s minimum support price by 10–20% since October 2024, discouraging plantings even as the southwest monsoon forecast is above average. Compounding the bearish sentiment, soymeal demand has weakened, with the poultry industry turning to cheaper DDGS feed. As a result, India’s edible oil import bill is set to rise, with potential implications for global oilseed trade flows and prices. Market participants are watching weather patterns, global crop prospects, and Indian policy responses closely as the season unfolds.

Exclusive Offers on CMBroker

Soybeans

yellow, organic

99.8%

FOB 0.80 €/kg

(from CN)

Soybeans

yellow

99.5%

FOB 0.70 €/kg

(from CN)

Soybeans

No. 2

FOB 0.60 €/kg

(from US)

📈 Prices

| Origin | Type | Purity | Organic | Location | Delivery Terms | Latest Price (USD/kg) | Previous Price (USD/kg) | Update Date | Market Sentiment |

|---|---|---|---|---|---|---|---|---|---|

| China | Yellow, Organic | 99.8% | Yes | Beijing | FOB | 0.70 | 0.67 | 2025-05-27 | Bullish |

| China | Yellow | 99.5% | No | Beijing | FOB | 0.63 | 0.59 | 2025-05-27 | Bullish |

| USA | No. 2 | – | No | Washington D.C. | FOB | 0.33 | 0.33 | 2025-05-22 | Neutral |

| India | Sortex Clean | – | No | New Delhi | FOB | 0.71 | 0.71 | 2025-05-22 | Stable |

| Ukraine | – | – | No | Odesa | FOB | 0.36 | 0.37 | 2025-05-22 | Bearish |

🌍 Supply & Demand

- India: Soybean acreage is projected to shrink as farmers switch to corn and sugarcane, driven by higher returns and sustained low soybean prices.

- Domestic Output: Likely to fall substantially in 2025, increasing India’s dependence on imported edible oils.

- Import Demand: India will continue as the world’s leading edible oil importer, sourcing palm oil from Indonesia/Malaysia and soya/sunflower oil from Argentina, Brazil, Russia, and Ukraine.

- Soymeal: Local demand is weakening as poultry producers prefer DDGS, which is over 30% cheaper than soymeal.

- Global Market: Any supply shortfall in India could tighten global soya oil and meal supplies, supporting international prices.

📊 Fundamentals

- USDA Reports: Recent WASDE reports highlight stable US soybean acreage, but weather remains a risk in the Midwest.

- Speculative Positioning: Managed money has increased long exposure on US exchanges, anticipating tighter global supplies.

- Inventories: Global ending stocks are forecast slightly lower year-on-year, with Brazil and Argentina still holding large surpluses, but Indian drawdown could alter trade flows.

- Price Trends: Chinese and Indian FOB soybean prices are trending higher, while US and Ukrainian prices remain relatively soft.

⛅ Weather Outlook

- India: The 2025 monsoon is forecast to be above average, but the benefit is limited as many farmers are switching away from soybeans.

- US Midwest: Weather is currently favorable, but June-July moisture will be critical for yield formation.

- South America: Brazil and Argentina have completed harvests with robust yields, but dry conditions in southern Brazil could affect second-crop corn, indirectly supporting soybean prices.

🌐 Global Production & Stocks

| Country | 2024/25 Production (Mt) | 2024/25 Ending Stocks (Mt) | Change vs. 2023/24 |

|---|---|---|---|

| Brazil | 153.0 | 37.5 | +1.5% |

| USA | 113.0 | 8.7 | +0.7% |

| Argentina | 51.0 | 5.8 | +3.2% |

| India | 10.5 (est.) | 0.8 | -15% |

| China | 20.2 | 0.2 | +1.0% |

📆 Trading Outlook & Recommendations

- Producers: Indian growers should monitor government support policies and weather, but diversification into alternative crops appears justified in the current price environment.

- Importers: Indian oilseed crushers and edible oil refiners should secure forward contracts for soya and sunflower oil as import demand is likely to rise.

- Exporters: South American and US exporters can expect firmer demand from India, especially for refined soya oil and meal.

- Speculators: Watch for upward price moves on CBOT and Dalian in response to Indian acreage news and any adverse US Midwest weather in coming weeks.

- Risk: Volatility will remain high through the Indian monsoon and US growing season; consider using options for price protection.

🔮 3-Day Regional Price Forecast

| Exchange/Location | Current Price (USD/kg) | 3-Day Forecast | Sentiment |

|---|---|---|---|

| CBOT (US No. 2) | 0.33 | 0.33–0.35 | Neutral/Bullish |

| FOB Beijing (CN Yellow, Organic) | 0.70 | 0.71–0.73 | Bullish |

| FOB New Delhi (IN Sortex Clean) | 0.71 | 0.72–0.74 | Bullish |

| FOB Odesa (UA) | 0.36 | 0.36–0.38 | Neutral |