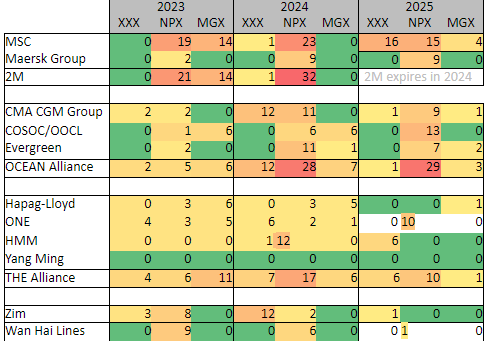

Megamax new buildings to phase into the Asia – Europe trades

The top-11 container lines are scheduled to receive another 89 large container vessels in the remaining course of the year. This number includes 31 megamax (MGX), 41 neopanamx (NPX) and 9 ‘other’ mainline vessels (XXX) larger than 7’000 TEU. Depending on market demand, delivery of some of these ships could be deferred to next year.

The delivery wave will start rolling on 14 March, when the 24’116 TEU MSC TESSA will join the ‘AE6/Lion’ service at Ningbo. Upon delivery, the vessel is expected to become the world’s largest container ship – but only for a few days. The 24,188 TEU OOCL SPAIN will take over this title on 18 March when it will leave Shanghai to join the Far East-North Europe ‘LL3’ loop on 21 March, before passing the crown to the 24’346 TEU MSC IRINA which is to join the Asia–Med ‘AE10/Jade’ service on 21 March in Qingdao.

The first two sister ships of the MSC TESSA will follow her soon. The 24,116 TEU MSC CELESTINO MARESCA will join her sister in the fleet of the “AE6/Lion” loop on 28 March in Ningbo, while the MSC RAYA will start her maiden voyage on 9 April in Shanghai for the “AE55/Griffin” service. Also, in April will Hapag-Lloyd’s 23’666 TEU BERLIN EXPRESS, the first of 12 LNG-powered megamaxes for the carrier, join one of THE Alliance’s Far East–North Europe loops.

The new megamax ships will hit the market at a time of weakening demand on the main East–West trades.

Market outlook March 2023

Ocean Freight rates – Asia-Pacific exports

ASPA-EURO: The blank sailing program continues after CNY break to balance out demand and supply.

ASPA-AMNO: The port situation globally is improving on both the East and West Coast with vessel dwell decreasing week over week due to softening demand. The volume recovery in March remains slow and carriers are looking for more support.

ASPA-AMLA: After February’s blank voyage program and waves of GRI, the rate level of both the East Coast and West Coast had been pulled up by 70-90% compared to the pre-CNY level. Capacity will resume to 100% in March, the market is expecting the rates in 1H to be maintained as the rolling pool effect, and subsequently coming down in 2H March. Caribbeans including Panama is open in March.

ASPA-MENAT: Middle East markets are facing a strong volume surge in view of the early Eid holidays this year. Coupled with blank sailings starting from Pre Lunar New Year, GRIs are taking place strongly for the Gulf/Red Sea markets. East MED market is affected by blank sailing programs, especially from The Alliance but extra loaders deployed by non-Alliance members are counterbalancing capacity thereby diminishing the possibility of immediate GRIs. However, stronger forecasts to TR/IL can be seen from customers from mid-Feb onwards which could see GRI possibility from March.

The earthquake in TR/SY is affecting South-Eastern ports and Iskenderun is now not operational until further notice.

African markets are lull but more blank sailings are taking place from carriers to stop rate erosion. In general, March’s outlook shows signs of a volume surge, especially for Middle East markets.

ASPA-ASPA: Rate continues to slide but at a much slower pace as the capacity of several locations had been reported tight. This resulted from the CNY blank sailing arrangements where roll pools were accumulated at origin and transshipment ports. Time-sensitive cargoes are recommended to load on direct service to prevent any potential delay at the transshipment port. In general, carriers have a positive outlook in the coming months with CN resuming production post CNY.

Market outlook March 2023

Ocean Freight rates – Other major trades

EURO-AMNO: Ports in Europe and North America remain fluent. The inland transport situation in Europe is generally sufficient but a series of strikes in various countries may lead to short-term disruptions and impact productivity. Even though the overall situation improved significantly, capacity constraints within the rail yards and chassis shortages still occur throughout the US. Seasonal weather delays have to be expected for truck and rail moves in Canada and the US. Load weight restrictions (Spring Thaw Regulation) will come into effect as of March 6th, 2023 for all truck moves within or through to province of Quebec. Schedule integrity improved further as less port omissions are seen since the vessels are catching up to their original schedule. Vessel space is generally available on short notice but can be tight on certain departures.

EURO-ASPA+MEA

Asia: The space situation is still relaxed. No issues with capacity, only vessel delays, even though a high number of blank sailings in March are expected. Rates are still decreasing slightly and are on a very low level.

AU/NZ: No space issues any longer and decreasing rates on both services.

MEA: Space is OK. Rates are decreasing slightly. No issues with equipment. Capacities into East Med available and rates soften for short- and long-term contracts.

AMNO-EURO: The FAK rates are now stable after seeing some reductions in Jan/Feb. There is no change in capacity. Schedules and services are now returning to some normalcy.

AMNO-ASPA: Rates are very stable. Capacity is up and carriers are actively looking for freight.

AMLA Exports

AMLA – AMNO & INTRA: NAC short-term/long-term pricing is flexible with free time conditions. Spot pricing is very fluid, with aggressive levels ex BR & MX in particular. Space is opening up and readily available. Carriers monitoring heavily allocation use & ‘no show’ bookings. Booking forecasts remain mandatory.

AMLA – ASPA: Good space availability, due to low demand. Stable rates for the same reason.

AMLA – EURO, MENAT & SSA: Mexico exports to N. Euro, Med and Mideast have softened. Vessels are open. In the middle of the contracting season, SAEC market continues the fast, downwards trend to EURO and Med. Rates are back to pre-Covid levels. Only Central America exports and trades to Africa remain at high levels.

Economic outlook & demand evolution – The global economy moves forward,

averting recession

Europe: The eurozone may avert a recession, but economic conditions remain challenging. Owing to mild winter weather, high natural gas storage levels, and falling energy prices, the risk of a severe recession has been averted. Consumer and business sentiment has improved. Despite easing, consumer price inflation remains high, at 8.5% YoY in January, eroding household incomes. Rising interest rates, tightening credit standards, and housing market corrections will impede near term grow.

Americas: The US economy enters 2023 with a new burst of energy. In January, the unemployment rate fell to 3.4%, its lowest level since May 1969. After declines in November and December, retail sales and manufacturing production posted strong rebounds in January. IHS Markit’s latest US GDP tracking suggests that real GDP will decrease at a modest 0.5% annual rate in the first quarter of 2023, pulled down by a sharp reduction in inventory accumulation and further declines in residential construction and business equipment investment. Consumer spending remains on a slow growth path, supported by rising employment and savings

accumulated during the pandemic but restrained by rising interest rates and rising debt. After 2.1% growth in 2022, we project US real GDP to increase 0.7% in 2023 and 1.6% in 2024.

Asia Pacific: Asia Pacific will lead all regions in growth as mainland China re-opens. The shift in policy focus from zero-COVID to economic stimulus has advanced mainland China’s growth. Tourism surged during the Lunar New Year holidays. However, manufacturing activity has remained sluggish, weak export demand. Consumers remain cautious, saving at a high rate and refraining from large purchases that require financing. Real GDP growth should pick up to 5.6% in 2024 before resuming a long-run deceleration.

Although growth in other parts of Asia Pacific will moderate in 2023, IN, VN, PH, & KH will achieve real GDP growth rates above 5.0%. However, tightening financial conditions and downturns in segments of the electronics industry will lead to more subdued growth in KR, TW, MY, AU, & NZ.

Emerging & Developing Countries: The Middle East and North Africa (MENA) region’s growth outlook remains a tale of two halves. With the oil price remaining at around USD90 per barrel and the global outlook for oil demand reasonably solid, the region’s oil exporters expect robust growth in 2023 and 2024. In contrast, several oil-importing countries, including Egypt and Tunisia, are confronted with a difficult global financial environment and expect growth to slow in the near term.

Demand Development: In January, the JPMorgan Global Composite Output Index (compiled by S&P Global) climbed 1.6 points to 49.8, signaling a stabilization in economic activity. The global services PMI™advanced 2.0 points to 50.1, while manufacturing PMI™edged up 0.4 points to 49.1. Input costs accelerated, while output price inflation continued to ease.

Source: DGF Global Forwarding