Mustard seed and mustard oil prices in India have turned decisively higher as mills accelerate procurement into a rising global vegetable oil and crude oil market, with a weak rupee amplifying the cost support. The near-term setup is clearly bullish, with domestic seed values underpinned by strong oil demand despite a modest increase in 2025–26 rabi output.

Indian mustard, a cornerstone of the domestic edible oil complex, is tightening as branded mills step up buying to pre-empt further cost escalation. Local benchmarks in Rajasthan and key refining hubs have reacted immediately to a sharp rally in palm and soybean oil, driven by spiking crude oil prices amid Middle East conflict. At the same time, a softer rupee is raising import costs for competing oils, making domestically crushed mustard oil more attractive. Export-oriented buyers, especially in Europe, should prepare for sustained upward pressure into mid-April.

Exclusive Offers on CMBroker

Mustard seeds

yellow, bold, sortex

99.95%

FOB 0.99 €/kg

(from IN)

Mustard seeds

yellow, micro, sortex

99.95%

FOB 0.89 €/kg

(from IN)

Mustard seeds

brown, micro, sortex

FOB 0.82 €/kg

(from IN)

📈 Prices & Benchmarks

Mustard seed and oil prices across major Indian centres have firmed in response to stronger mill procurement and a tightening global vegoil balance. At Jaipur, the key pricing point in Rajasthan, conditioned mustard gained about EUR 1.06 per quintal to roughly EUR 79.18 per quintal, reflecting renewed buying by large branded processors. Mustard oil (cold-pressed kachi ghani) in Jaipur moved up by roughly EUR 3.19 per quintal to around EUR 160.46 per quintal on reduced seller activity.

In other hubs, Delhi’s Dadri corridor is quoting mustard oil near EUR 157.28 per quintal, while Mumbai expeller-grade values have softened marginally to about EUR 158.34 per 10 kg, suggesting some regional variation in margins. Kolkata kachi ghani is holding near EUR 167.90 per 10 kg, with Admapur wholesale offers clustered around EUR 163.02–163.55 per 10 kg. Export-grade Indian mustard seeds on an FOB New Delhi basis remain broadly stable in late March, with yellow bold sortex at about EUR 0.99/kg, yellow micro sortex around EUR 0.89/kg, and brown types at EUR 0.73–0.82/kg, indicating firm but not yet runaway seed values.

| Product / Location | Latest Level (EUR) | Unit | Trend (late March) |

|---|---|---|---|

| Mustard seed, conditioned, Jaipur | ≈ 79.18 | per quintal | Firm, +1.06 EUR |

| Mustard oil, kachi ghani, Jaipur | ≈ 160.46 | per quintal | Firm, +3.19 EUR |

| Mustard oil, Delhi (Dadri) | ≈ 157.28 | per quintal | Firm |

| Mustard oil, kachi ghani, Kolkata | ≈ 167.90 | per 10 kg | Steady at high levels |

| Mustard seeds, yellow bold, FOB New Delhi | 0.99 | per kg | Stable vs. previous offers |

| Mustard seeds, yellow micro, FOB New Delhi | 0.89 | per kg | Stable |

| Mustard seeds, brown bold, FOB New Delhi | 0.73 | per kg | Stable |

| Mustard seeds, brown micro, FOB New Delhi | 0.82 | per kg | Stable |

🌍 Supply & Demand Drivers

India’s 2025–26 rabi mustard crop is projected to rise modestly, providing a fundamentally comfortable but not burdensome supply backdrop. The Solvent Extractors’ Association of India pegs output around 11.94 million tonnes, up roughly 3.65% year-on-year from 11.52 million tonnes, supported by expanded sowing of about 9.391 million hectares versus 9.215 million hectares previously. Rajasthan remains the powerhouse with an estimated 5.39 million tonnes, followed by Uttar Pradesh at 1.81 million tonnes and Haryana at 1.27 million tonnes; only Madhya Pradesh shows a slight decline to 1.39 million tonnes.

Despite the larger harvest, the demand side is tightening the balance. Branded oil mills are aggressively replenishing seed inventories to cover forward crushing programmes amid rising replacement costs for imported palm and soybean oil. The reduction in spot seller activity, particularly in premium kachi ghani grades, is amplifying the firmness in oil prices, even as seed offers remain measured. Domestic consumers and food processors are thus facing a phase of cost pass-through just as festival and wedding-related demand begins to pick up in parts of India.

📊 External Markets & Currency Impact

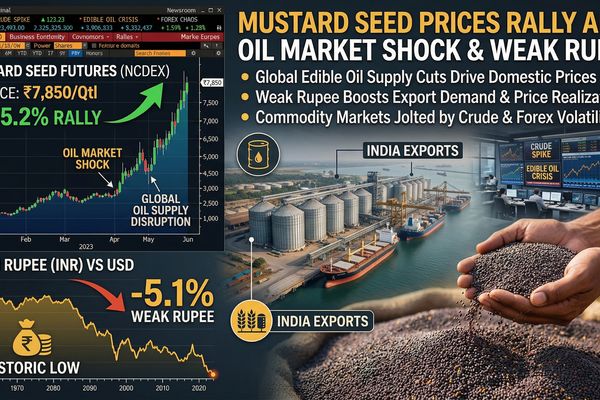

The current mustard complex is being driven less by domestic oversupply and more by a global energy and vegoil shock. Crude oil has spiked to around EUR 110 per barrel as the ongoing US–Iran–Israel conflict disrupts tanker traffic and tightens global energy logistics. Elevated crude values are supporting biodiesel economics, which in turn are pulling up palm and soybean oil prices. Indonesian crude palm oil is trading near EUR 1,280 per tonne, roughly EUR 100 higher in a short time window, while Malaysian CPO futures for June delivery have jumped by about 141 ringgit to 4,772 ringgit per tonne.

India has further reinforced this support via administrative and currency channels. The government has raised the import tariff value for crude palm oil to about EUR 1,112 per tonne from EUR 1,103, marginally increasing the landed cost for refiners. At the same time, the rupee has weakened sharply from roughly 91 to 94.70 per US dollar through March, significantly increasing the domestic currency cost of all imported vegetable oils. This combination makes domestic mustard oil relatively more competitive, incentivising mills to lock in local seed supplies at today’s levels before a further up-leg in prices.

🌦 Weather & Crop Outlook

With the 2025–26 rabi crop largely set, short-term weather plays a secondary role compared with macro and currency forces. However, near-term conditions in North and Central India remain broadly supportive for harvesting and post-harvest handling, reducing the risk of quality losses. The key forward-looking variable is not yield but milling pace and storage behaviour: as mills accelerate crushing to meet strong edible oil demand, the availability of free seed stocks in mandis is likely to tighten, reinforcing the current firm undertone.

📆 Short-Term Forecast & Trading Outlook

The two-to-four-week outlook for mustard seeds and mustard oil is clearly bullish. The interaction between higher global edible oil benchmarks, elevated crude oil, a weaker rupee and only moderately larger Indian production provides a solid price floor. Any temporary dips linked to harvest pressure are likely to be shallow and short-lived as mill demand quickly absorbs available volumes. European buyers of Indian mustard oil and derived products should budget for continued cost escalation at least through mid-April.

- Indian crushers and refiners: Consider advancing seed procurement and hedging a larger portion of Q2 requirements while FOB seed offers remain below EUR 1.00/kg for yellow bold grades; downside appears limited given external price drivers.

- European and global importers: Front-load purchases of Indian mustard oil and seed where possible, or diversify timing across the next 2–4 weeks to average into a rising market rather than waiting for pullbacks that may not materialise.

- Producers and traders in India: Maintain a measured selling pace; holding quality stocks could be rewarded as crude and vegoil markets remain volatile on geopolitical risks.

📉 3-Day Directional Price Indication (EUR)

- FOB New Delhi mustard seeds (yellow, bold/micro; brown types): Slightly firmer bias (0.5–1.5% up) as export and domestic crushing demand absorb arrivals.

- Mustard oil, kachi ghani (Jaipur, Kolkata): Firm to higher (1–2% upside risk) on tight seller interest and strong mill coverage buying.

- Mustard oil, expeller grade (Mumbai, Delhi): Mostly steady to mildly firmer, tracking global vegoil futures and local currency moves.

Related posts:

Indian mustard seed rally underpinned by strong mill demand and firmer vegoils

Indian mustard seed rally underpinned by strong mill demand and firmer vegoils

Cumin Market Caught Between Tight Indian Supply and Geopolitical Shock

Cumin Market Caught Between Tight Indian Supply and Geopolitical Shock

Indian Mustard Seed Rally Tightens Global Cold-Pressed Oil Market

Indian Mustard Seed Rally Tightens Global Cold-Pressed Oil Market

Mustard Seed Market: Seed Weakness vs. Firm Oil Prices Creates Window for Buyers

Mustard Seed Market: Seed Weakness vs. Firm Oil Prices Creates Window for Buyers

Indian Mustard Seed Prices Ease as Oil Mills Step Back from Buying

Indian Mustard Seed Prices Ease as Oil Mills Step Back from Buying