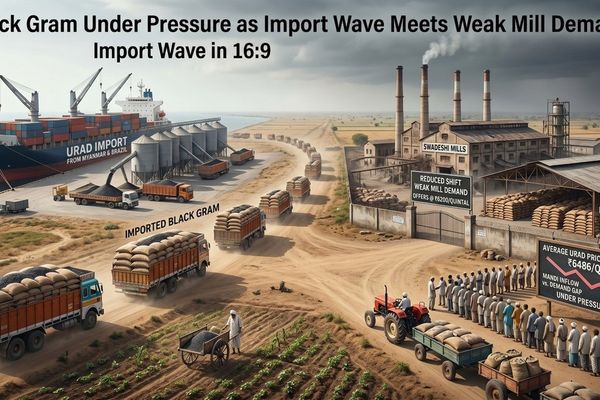

Black gram prices have fallen for the second consecutive day, pressured by softer import offers and weak dal mill demand even as India moves through a seasonal consumption peak. With domestic spot values trading below the government MSP and import flows from Myanmar and Brazil remaining active, the near-term tone stays weak to slightly negative.

Black gram, a key input for urad dal, is struggling to clear current supply as mills remain cautious and import prices at Chennai keep easing. Myanmar CIF values continue to trend lower, feeding directly into port and inland markets, while rabi-season arrivals in Andhra Pradesh and early summer crop inflows from Madhya Pradesh and Gujarat add to available stocks. Some early improvement in demand for processed mogar and gota is emerging, but this has not yet translated into a broad-based recovery in mill buying. For now, the market is stuck with an uncomfortable supply overhang and only modest demand signals.

📈 Prices & Spreads (in EUR)

Indicative spot and import prices converted at ~0.011 EUR per rupee and ~0.011 EUR per USD-equivalent for comparative purposes:

| Market / Grade | Price Range | Approx. Price (EUR/quintal) | Direction (Day-on-day) |

|---|---|---|---|

| Chennai port, FAQ (May–Jun) | ₹7,800–7,820 | €0.90–0.90 | ▼ −₹50 |

| Chennai port, SQ (May–Jun) | ₹8,090–8,095 | €0.98–0.98 | ▼ −₹25 |

| Delhi, FAQ | ₹8,350–8,375 | €0.94–0.95 | ▼ −₹25 |

| Delhi, SQ | ₹8,990 | €1.02 | ▼ −₹25 |

| Mumbai, FAQ | ₹8,010 | €0.91 | ▼ −₹50 |

| Guntur, polished | ₹8,285–8,310 | €0.93 | ▼ −₹50 |

| Vijayawada | ₹8,345 | €0.93 | ▼ −₹25 |

| Kolkata | ₹8,285–8,310 | €0.93 | ▶ stable |

| Myanmar FAQ (CIF, May–Jun) | $815/t | ≈€8.97/quintal | Softening trend |

| Myanmar SQ (CIF, May–Jun) | $905/t | ≈€9.96/quintal | Softening trend |

| Brazil origin (CIF, Jun–Jul) | $870/t | ≈€9.57/quintal | ▶ steady |

| Government MSP (India) | ₹7,800 | ≈€85.80/t | Benchmark |

Domestic wholesale prices in major producing markets are trading below the Minimum Support Price (MSP) of ₹7,800 per quintal (~€85.80/t), underlining the bearish tone and potential pressure on farmer margins.

🌍 Supply & Demand Balance

The core imbalance in black gram lies in the combination of expanding import availability and lacklustre mill demand. Myanmar-origin FAQ and SQ grades are arriving at increasingly competitive CIF levels, exerting direct downward pressure on Chennai port quotes and, by extension, on inland markets such as Delhi, Mumbai, Guntur and Vijayawada.

At the same time, domestic supply is building. Summer rabi arrivals from Andhra Pradesh are flowing steadily, and harvesting of summer black gram in Madhya Pradesh and Gujarat has already started, with early volumes entering local markets. These inflows are expected to increase meaningfully by the end of May, coinciding with continued import arrivals and further weighing on the balance.

On the demand side, dal processing mills remain cautious despite the usual seasonal consumption peak. Weak procurement from mills is preventing the market from absorbing current supply, keeping inventories comfortable to heavy. The one constructive sign is a moderate improvement in inquiries for processed products such as black gram mogar and gota splits, which could gradually support offtake if the trend strengthens.

📊 Fundamentals & Policy Context

The MSP for black gram is set at ₹7,800 per quintal, yet wholesale prices in key producing belts are still under this benchmark. This situation highlights a structurally soft market where policy support has not been strong enough, or broad enough, to lift cash prices to the official floor.

Softening Myanmar export offers have been a persistent driver of the current downturn. As overseas sellers adjust to global demand conditions and currency moves, their lower offers are quickly transmitted to Indian CIF values, which then cap any domestic price recovery attempts. Brazil-origin shipments for June–July remain steady, but they add another source of competition for Indian growers and domestic stockholders.

Without a decisive pickup in mill demand or a policy-induced tightening of import flows, local fundamentals are likely to stay heavy into late May. The recent two-day price slide is therefore less a short-term correction and more a reflection of an underlying surplus environment.

🌦 Weather & Crop Outlook

Weather for key black gram producing states – Andhra Pradesh, Madhya Pradesh and Gujarat – will be closely watched as summer harvesting progresses and preparations for the next sowing cycle begin. Normal to slightly above-normal temperatures with adequate pre-monsoon showers would support yield prospects and encourage planting, potentially reinforcing the current supply-heavy backdrop.

Conversely, any emerging concerns over excessive heat or delayed pre-monsoon rains could temper production expectations and offer some medium-term support. At present, however, physical flows from the rabi and summer crops are strong enough that modest weather-related risks are secondary to the dominant import and demand dynamics.

📆 Short-Term Price Outlook (2–3 Weeks)

- Bias remains soft to sideways, with prices seen as range-bound to slightly lower across major Indian markets over the next two to three weeks.

- Downside risks stem from continued softening of Myanmar CIF offers, rising arrivals from Andhra Pradesh, Madhya Pradesh and Gujarat, and ongoing mill buying reluctance.

- Upside potential hinges on either a meaningful pickup in dal mill procurement – possibly triggered by improved retail demand for processed urad products – or a slowdown in import bookings and shipments.

- Below-MSP spot prices limit farmer selling appetite at lower levels, which may help create a tentative floor, particularly if government procurement or trade policy support is enhanced.

📌 Trading & Procurement Guidance

- Dal mills / processors: Consider staggered, hand-to-mouth buying strategies to capitalise on potential further softening, while gradually adding coverage if mogar and gota demand continues to improve.

- Importers / traders: Monitor Myanmar offer trends closely; avoid over-committing at current CIF levels given the risk of additional downside if global pulses sentiment softens further.

- Farmers and local stockists: Below-MSP prices argue for cautious selling; where storage and cash-flow permit, holding limited quantities may be justified in expectation of policy support or a marginal recovery once peak arrivals pass.

- End users / food manufacturers: Current weakness offers an opportunity to lock in part of Q2–Q3 needs at attractive basis levels, but retain flexibility in case prices drift lower on heavier arrivals.

📉 3-Day Directional Outlook (Key Hubs, in EUR)

- Chennai port (FAQ/SQ): Mild downside bias; prices likely to test slightly lower levels in EUR terms if Myanmar CIF offers remain soft.

- Delhi & Mumbai: Range-bound to marginally weaker, tracking port prices and local arrivals; spreads between FAQ and SQ to remain relatively stable.

- Guntur, Vijayawada & Kolkata: Mostly steady to slightly lower; Kolkata may continue to outperform marginally given its recent stability, while southern markets reflect increased rabi and summer inflows.

Related posts:

China Lentils: Weak Exports, Firm Import Demand and Sideways Prices

China Lentils: Weak Exports, Firm Import Demand and Sideways Prices

Lentils Market Steady to Soft as Indian Green Gram Stocks Cap Upside

Lentils Market Steady to Soft as Indian Green Gram Stocks Cap Upside

Lentil Market Caught Between Firm Import Costs and Softer Mill Demand

Lentil Market Caught Between Firm Import Costs and Softer Mill Demand

Lentil Market Steady While Indian Black Gram Tightens Import Arbitrage

Lentil Market Steady While Indian Black Gram Tightens Import Arbitrage

Lentil Market Steady as Indian Black Gram Stays Soft but Well Supplied

Lentil Market Steady as Indian Black Gram Stays Soft but Well Supplied

Lentil Market Holds Steady as Indian Green Gram Stocks Cap Upside

Lentil Market Holds Steady as Indian Green Gram Stocks Cap Upside

Lentil Market Steady as Indian Green Gram Signals Comfortable Pulse Supply

Lentil Market Steady as Indian Green Gram Signals Comfortable Pulse Supply

Indian Lentils Extend Rally as Tight Rabi Supply Meets Firm Import Floor

Indian Lentils Extend Rally as Tight Rabi Supply Meets Firm Import Floor