Danone & Nestlé Lag Consumer Staples in Early 2026 as Portfolio Reshuffle Intensifies

CMB News | Corporate & Consumer | February 2026

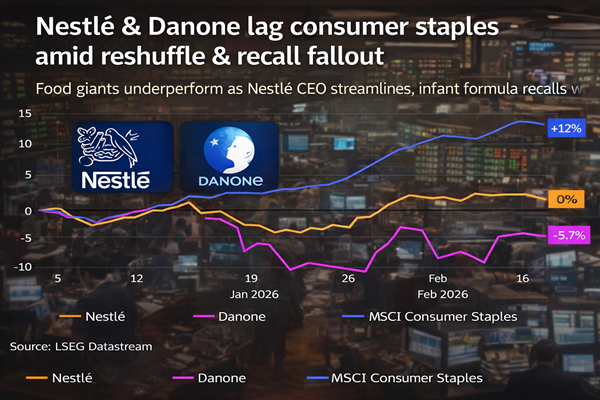

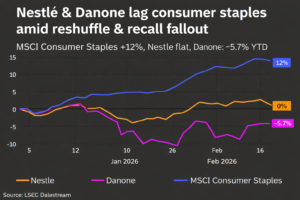

Shares of Nestlé and Danone have underperformed the broader consumer staples sector in early 2026, weighed down by infant formula recalls and ongoing portfolio restructuring. While the MSCI Consumer Staples Index is up roughly +12% year-to-date, Nestlé is flat and Danone remains negative at around –5.7%, highlighting investor caution toward the two European food giants.

📊 Market Performance Snapshot (YTD 2026)

-

MSCI Consumer Staples Index: +12%

-

Nestlé: ~0%

-

Danone: –5.7%

Underperformance reflects both operational challenges and strategic realignment moves.

🍦 Nestlé Expands Asset Disposal Program

Nestlé announced it is in advanced talks to sell its remaining in-house ice cream business (≈ CHF 1 billion in annual sales) to Froneri, its existing joint venture partner. The assets span Canada, Chile, Peru, Malaysia, China, and Thailand and include brands such as KitKat Ice Cream and Coffee Crisp.

This follows:

-

Planned exit from vitamin & supplement brands

-

Gradual deconsolidation of the waters business by 2027

-

Ongoing restructuring under CEO Philipp Navratil, including 16,000 job cuts

Nestlé maintains its 50% stake in Froneri (valued at ~€15 billion including debt) and is prioritizing core categories: coffee, petcare, nutrition, and food/snacks.

💬 Strategic Rationale

Navratil described the ice cream unit as “strong, but small, and a distraction,” reinforcing a sharpened focus on high-margin, scalable segments.

🍼 Infant Formula Recall: Temporary Headwind

Nestlé’s turnaround has been overshadowed by a major infant formula recall:

-

Estimated CHF 200 million one-off sales impact

-

Approx. –20 basis points hit to 2026 volumes

-

CFO indicates broader consumer impact remains uncertain

While management claims reputational trust remains intact, the Gerber brand continues to underperform, with Navratil publicly stating dissatisfaction with its market share trajectory.

📈 Operational Performance: Stabilizing Fundamentals

Despite headline risks:

-

Q4 organic sales growth: +4%

-

Price: +2.8%

-

Real Internal Growth (RIG): +1.3% (vs. 0.9% expected)

-

-

2026 organic growth guidance: 3–4%

-

Operating margin (2025): 16.1%, with expected improvement in 2026

-

RIG expected to exceed 2025’s 0.8%

Nestlé’s ability to protect pricing and stabilize volumes suggests fundamentals are improving, even as restructuring continues.

🥛 Danone: Ongoing Sector Pressure

While less detail is provided in this update, Danone’s negative share performance reflects similar challenges:

-

Infant formula-related sector scrutiny

-

Slower volume growth

-

Competitive pricing pressures

-

Exposure to premium dairy categories facing consumer trade-down

🔎 CMB Outlook

Nestlé’s strategic disposals indicate a clear pivot toward simplification and capital discipline, aligning with broader industry trends (e.g., Unilever’s Magnum Ice Cream spin-off in 2025). However, execution risk remains high.

Key watchpoints:

-

Speed and valuation of asset sales (ice cream, vitamins, water)

-

Recovery trajectory in infant nutrition

-

Margin expansion amid FX volatility and tariff risks

-

Volume growth stabilisation in core categories

Bottom line:

Nestlé’s fundamentals are stabilising, but markets are waiting for proof of consistent execution. Danone faces similar structural headwinds, keeping both names behind the broader consumer staples rally.

Source: Reuters