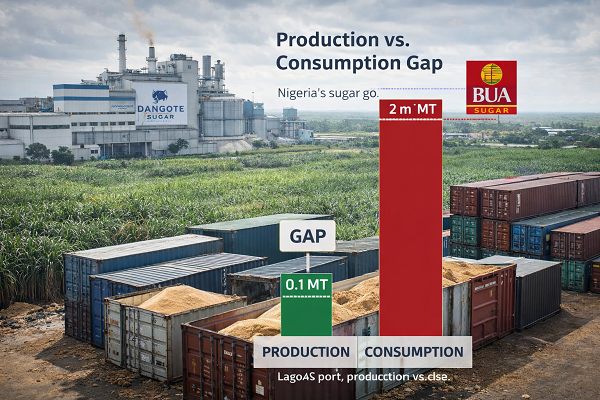

Nigeria’s sugar sector remains mired in a structural crisis that successive government initiatives have so far failed to resolve, with domestic production continuing to meet less than five percent of national consumption and the country’s dependence on imports deepening year after year. A new Sugar Annual report published on March 19, 2026 by the United States Department of Agriculture’s Foreign Agricultural Service in Lagos paints a sobering picture of a sector held back by high production costs, chronic infrastructure deficits, limited private investment, and fifteen years of policy underperformance under the country’s flagship sugar development programme.

For marketing year 2025/26, sugarcane production is forecasted at 3.5 million metric tons — unchanged from the prior year — while sugar imports are projected to rise to 2.03 million metric tons to fill the enormous gap between what Nigeria produces and what its growing population and expanding food processing industry consume. With consumption forecast to reach 1.7 million metric tons in the current marketing year and rising to 1.8 million metric tons in 2026/27, the structural imbalance at the heart of Nigeria’s sugar economy shows no meaningful sign of improvement despite more than a decade of government-mandated backward integration policies.

Sugarcane Production Stagnant as Structural Barriers Persist

Nigeria’s sugarcane production has remained effectively flat for years, and the USDA’s latest forecasts confirm that no improvement is expected in the near term. For marketing year 2025/26, sugarcane production is estimated at 3.5 million metric tons across a harvested area of 100,000 hectares — figures that are unchanged from the previous year and reflect a sector that is treading water rather than moving forward.

The reasons for this stagnation are deeply structural and well-documented. High operational costs for planting, irrigation, agrochemicals, and labour continue to deter expansion, particularly among the smallholder farmers who actually account for approximately 70 percent of sugarcane cultivation in Nigeria. These small-scale producers grow primarily soft chewing cane — informally consumed raw for its juice or processed into crude sugar products — rather than the industrial-grade cane that the country’s major refineries require as feedstock. The remaining 30 percent of sugarcane production comes from the country’s three major industrial players — Dangote Sugar Refinery, BUA Sugar Refinery, and Golden Sugar Refinery — who are responsible for virtually all of Nigeria’s commercially processed sugar output.

The challenges facing small-scale farmers are compounding and interconnected. Lack of access to improved cane varieties, near-total dependence on rain-fed production without irrigation infrastructure, minimal use of modern agricultural practices, limited access to credit facilities, and the absence of meaningful government support for technology adoption have collectively kept yields far below their potential. The USDA report notes that smallholder farmers do not have access to improved varieties, and their production methods remain largely unchanged from previous decades.

Nigeria’s major sugarcane-producing states — Kaduna, Niger, Kano, and Adamawa — have the agro-climatic conditions to support significantly higher production, but the enabling environment required to unlock that potential has not been created. Infrastructure deficits in electrical power, fuel supply, road networks, and agricultural machinery continue to inflate operational costs and reduce the commercial viability of expanding sugarcane cultivation across these states.

The Backward Integration Programme: Fifteen Years of Underdelivery

The centrepiece of Nigeria’s sugar development strategy for the past fifteen years has been the National Sugar Master Plan and its associated Backward Integration Programme, which officially commenced in January 2013. The core logic of the BIP is straightforward — companies that wish to import raw sugar into Nigeria must commit to developing and expanding domestic sugarcane cultivation in exchange for import quotas. The idea was to use the commercial incentive of import access to drive private sector investment in domestic production.

When the BIP was launched, the policy worked reasonably well as an incentive mechanism. Major players were motivated to expand their harvested areas in order to qualify for higher import quotas, and there was genuine momentum toward building out domestic production capacity. However, the government’s failure to deliver on its promised support for infrastructure development — particularly irrigation systems for sugar plantations — steadily undermined the programme’s commercial logic.

The results have been deeply disappointing. The NSMP was originally designed to eliminate Nigeria’s dependence on sugar imports entirely by 2020 through a staged expansion of domestic production. That target has been missed by an enormous margin. Domestic sugar production currently contributes less than five percent of total national consumption — a figure that represents only a marginal improvement from production levels recorded in 2010, when the master plan was still in its conceptual stages. Nigeria today remains just as dependent on imported sugar as it was when the BIP was launched, despite fifteen years of policy effort and hundreds of millions of dollars in private sector investment commitments.

In August 2025, the Nigerian Sugar Development Council signed new agreements with four operators to develop projects aimed at producing 400,000 metric tons of sugar annually as part of the second phase of the NSMP. While this represents a renewed push to revitalise the programme, industry analysts and USDA contacts express cautious scepticism given the long history of implementation failures that has characterised the first phase of the plan.

The major industrial players — Dangote, BUA, and Golden Sugar — have reportedly indicated that they plan to maintain the same planted area in the next marketing year, with little incentive to expand given low returns on investment and the continued absence of meaningful government support for infrastructure development. This is a significant departure from the early years of the BIP, when the prospect of higher import quotas was sufficient to motivate expansion. Today, that commercial incentive has been effectively neutralised by the combination of high costs and inadequate government delivery on infrastructure commitments.

Nigeria’s Major Refineries: Capacity Utilisation Remains Low

Nigeria’s three dominant sugar refining companies operate a combined installed refining capacity that, if fully utilised, would be more than sufficient to process the volumes required to significantly reduce the country’s import dependence. However, the gap between installed capacity and actual operational output tells the real story of the sector’s chronic underperformance.

Dangote Sugar Refinery and BUA Sugar Refinery each have an installed refining capacity of 1.5 million metric tons per year, while Golden Penny operates a smaller facility with capacity of 750,000 metric tons annually. Together, the three companies have a theoretical combined capacity of approximately 3.75 million metric tons per year — nearly double Nigeria’s current total sugar consumption.

In practice, however, both Dangote and BUA are operating at an estimated 50 percent of their installed capacity, reflecting the constraints imposed by inadequate domestic cane supply, infrastructure challenges, and the broader operational difficulties facing the sector. Golden Penny’s actual output falls in the range of 400,000 to 450,000 metric tons per year.

The three companies operate through distinctly different business models within the sugar value chain. Dangote is the only firm that processes locally grown sugarcane all the way through to finished white sugar, making it the closest to a fully integrated domestic sugar producer. Golden Sugar’s local processing ends at the raw sugar stage rather than producing refined white sugar. BUA, by contrast, operates primarily as a refiner of imported raw sugar rather than a processor of domestically grown cane — a model that makes it highly dependent on import quotas and the foreign exchange conditions that determine its ability to source raw sugar from international markets.

A new development noted in the USDA report is that additional players beyond the traditional three are beginning to enter the sugar refining space, which is expected to contribute incrementally to total sugar supply in the next marketing year — though the scale of this new entry is not yet sufficient to materially change the overall supply picture.

Imports Rising as Brazil Dominates Supply

With domestic production meeting less than five percent of consumption, Nigeria’s sugar supply chain is overwhelmingly dependent on imports — a dependency that is deepening rather than easing as consumption grows. For marketing year 2025/26, total sugar imports are forecast at 2.03 million metric tons, comprising 1.9 million metric tons of raw sugar and 130,000 metric tons of refined sugar imports measured in raw value equivalent. For marketing year 2026/27, total imports are projected to rise further to 2.13 million metric tons.

Brazil dominates Nigeria’s raw sugar import market with a commanding market share of over 97 percent, making Nigeria almost entirely dependent on a single origin for its primary sugar supply. According to Trade Data Monitor data cited in the USDA report, Nigeria imported 1.7 million metric tons of raw sugar in 2025 — a five percent increase compared to 2024 — driven by improvements in milling operations and easier access to foreign exchange for import payments.

Nigeria’s import policy framework is designed to protect the domestic refining industry while simultaneously trying to incentivise domestic cane production. The importation of refined sugar in retail packaging is completely banned. Only companies participating in the Backward Integration Programme — specifically Dangote Sugar Refinery, BUA Sugar Refinery, and Golden Sugar Company — are permitted to import raw sugar under the government’s quota system. Local companies involved in packaging and cubing sugar must source their refined sugar from domestic producers, or alternatively submit detailed multi-year demand projections to the government to justify any import requirements.

While these protectionist measures have successfully shielded domestic refiners from direct competition with imported refined products, they have not succeeded in their deeper objective of stimulating a meaningful expansion of domestic cane production. The result is a protected market in which imports of raw sugar continue to rise year after year while domestic production stagnates — the opposite of what the BIP was designed to achieve.

The recent stabilisation of the Nigerian naira and improvements in foreign exchange availability have been significant enabling factors in the import growth recorded over the past year. When the naira was under severe depreciation pressure in prior years, many BIP participants were unable to fully utilise their allocated import quotas because of the difficulty and cost of sourcing US dollars to pay for raw sugar purchases from Brazil. The easing of this foreign exchange constraint is now allowing quota holders to import closer to their allocated volumes, which is driving the uptick in total import figures.

Consumption Growth Driven by Food Processing and Demographics

On the demand side of Nigeria’s sugar equation, the outlook is considerably more positive than the supply picture. FAS-Lagos forecasts sugar consumption rising from 1.7 million metric tons in marketing year 2025/26 to 1.8 million metric tons in 2026/27 — a six percent increase driven by a combination of macroeconomic improvements, demographic expansion, and structural growth in the food and beverage processing sector.

The stabilisation of the Nigerian naira following a period of significant currency volatility, alongside improvements in consumer purchasing power and the broader macroeconomic environment, is supporting a recovery in consumer spending on food and beverage products. Food inflation has dropped sharply from 24 percent to 8.9 percent over the past year — partly reflecting the adoption of a new inflation calculation methodology — providing meaningful relief to Nigerian households and enabling greater consumption of sugar-intensive products.

Industrial consumption accounts for the overwhelming majority of Nigeria’s sugar demand, with the food processing, beverage, bakery, confectionery, and pharmaceutical sectors together accounting for approximately 80 percent of total sugar use. Household consumption of refined sugar in retail form accounts for the remaining 20 percent. The food processing industry is identified in the USDA report as the fastest-growing segment of the sugar value chain, with notable increases in consumption of bakery and confectionery items, soft drinks, and other processed food products. Major sugar buyers in the industrial segment include companies such as Cadbury, Dangote, and BUA.

Nigeria’s per capita sugar consumption currently stands at approximately nine kilograms per year — well below the African continental average of approximately 17 kilograms per year. This significant gap between Nigeria’s current per capita consumption and regional norms represents a substantial long-term demand growth opportunity, underpinned by Nigeria’s large and rapidly growing population, rising urbanisation rates, and an expanding working-age demographic that is expected to support higher discretionary spending on processed food and beverage products in the years ahead.

Policy Outlook: New Agreements Offer Hope but History Counsels Caution

The Nigerian government’s August 2025 agreements with four new operators to develop domestic sugar production capacity targeting 400,000 metric tons annually represent the most significant policy intervention in the sector in several years and signal a renewed commitment to the objectives of the National Sugar Master Plan under its second phase. If successfully implemented, these projects could begin to make a meaningful dent in Nigeria’s overwhelming import dependence — though the timeline for any such impact would extend well beyond the current marketing year.

However, the history of the NSMP’s first phase provides strong grounds for caution. The programme was designed fifteen years ago with ambitious targets that have consistently not been met, primarily because of implementation failures rather than flawed policy design. The government’s repeated inability to deliver on promised infrastructure support — particularly irrigation development — has been the central reason why private sector participants have not been able to expand production at the pace originally envisioned. Until this infrastructure delivery gap is addressed in a sustained and credible manner, the commercial incentives for expanding domestic sugarcane cultivation will remain insufficient to drive the scale of investment required.

The restriction of raw sugar imports to BIP participants and the ban on refined sugar imports continue to provide a degree of protection for the domestic refining industry, but these trade policy instruments alone cannot substitute for the infrastructure investment and smallholder farmer support that are ultimately necessary to transform Nigeria’s sugar production base. The sector’s 95 percent import dependency after fifteen years of backward integration policy is the clearest possible evidence that trade restrictions without complementary supply-side investment cannot achieve self-sufficiency objectives.

Market Outlook

Nigeria’s sugar market outlook for the next two to three years is characterised by rising consumption, stagnant domestic production, and growing import volumes — a combination that will keep the country deeply dependent on global raw sugar markets and particularly on Brazilian supply for the foreseeable future. The projected rise in total imports to 2.13 million metric tons in marketing year 2026/27 underscores the widening gap between domestic supply capacity and national demand.

For global sugar market participants, Nigeria represents a large and growing import market with stable and expanding demand fundamentals. Brazil’s near-total dominance of Nigeria’s raw sugar import market — with over 97 percent market share — leaves little room for alternative origins in the near term, though the entry of new refining players into the domestic market could gradually create some diversification of import sourcing over time.

The stabilisation of the naira and improvement in foreign exchange conditions are positive near-term factors that should enable BIP quota holders to more fully utilise their import allocations, supporting continued growth in import volumes. However, any renewed deterioration in Nigeria’s macroeconomic or foreign exchange environment could quickly reverse this trend and create supply disruptions for the country’s food processing and beverage sectors, which have become increasingly dependent on a steady and affordable supply of refined sugar as inputs to their production processes.