Green gram markets in India are holding steady in a narrow band, with heavy government buffer stocks and the ongoing summer harvest capping upside, while export-oriented lentil values from Canada and China soften slightly in euro terms.

The pulse complex is currently shaped by a notably bearish supply backdrop in green gram, where wholesale prices remain well below the official support level and fresh summer-crop arrivals from western India are beginning to build. At the same time, FOB offers for Canadian red and green lentils and Chinese small green types have eased marginally over the past three weeks, reflecting comfortable global availability and cautious buying interest. For the coming month, the main risk is not a sharp price break, but a prolonged sideways market that rewards disciplined, range-based strategies rather than directional bets.

Exclusive Offers on CMBroker

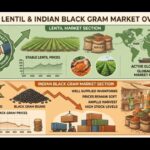

Lentils dried

Red football

FOB 2.55 €/kg

(from CA)

Lentils dried

Laird, Green

FOB 1.72 €/kg

(from CA)

Lentils dried

Eston Green

FOB 1.62 €/kg

(from CA)

📈 Prices & Market Mood

Across India’s main producing wholesale markets, green gram (moong) traded largely unchanged on Tuesday. Bold-grade lots in Indore, Madhya Pradesh, held around $83.95–85.95 per quintal, while chamki-grade in Jaipur was steady near $75.51 per quintal. Delhi quoted Rajasthan-line green gram between $73.43 and $80.78 per quintal, with Akola in Maharashtra reporting chamki-grade at about $88.16 per quintal. New-crop arrivals at Shirpur were priced in a wide $73.43–90.21 per quintal band, underscoring the influence of quality and moisture on early-season trades.

All of these values continue to sit below the government’s Minimum Support Price of roughly $91.95 per quintal, signalling a market still weighed down by ample domestic production and import competition. The discount to MSP is discouraging aggressive farmer holding, while traders are cautious about chasing any rally given the overhang of state-held stocks and the prospect of heavier summer arrivals by the end of May.

🌍 Supply & Demand Balance

The key feature on the supply side is the central government’s large buffer stock of green gram, currently the biggest among major pulses. This inventory functions as a ceiling on speculative activity: with official stocks readily available, traders see limited justification for building large private positions. Government procurement at the support price is ongoing in several states, but actual purchase volumes remain modest relative to total market arrivals, so the underlying burden of supply stays in private hands.

Weather has so far been favourable for the standing summer crop, and sowing in Madhya Pradesh and Gujarat has increased compared with last year. Harvesting is already under way in both states, with sporadic consignments entering wholesale markets. A more pronounced surge in arrivals is expected toward the end of May, which should keep spot prices contained and reinforce the current sideways pattern in the weeks ahead.

📊 Fundamentals & Price Relationships

Despite this heavy supply backdrop, demand from dal mills is described as steady and largely need-based. Processors are showing little urgency to step up coverage but are also not stepping back aggressively, in part because prices are already at a significant discount to the MSP. This combination argues against a deep price correction from current levels, even though any sustained rally looks unlikely before the full extent of summer-crop volumes is understood.

On the export side of the lentil complex, recent FOB offers indicate a mildly softer tone. Converting to euros at an indicative rate of 1 USD ≈ 0.93 EUR, Canadian red football lentils around 2.55 EUR/kg FOB Ottawa (down from about 2.60 EUR/kg in mid‑April), Canadian Laird green at roughly 1.60 EUR/kg (vs. 1.65–1.67 EUR/kg), and Eston green near 1.51 EUR/kg all suggest gentle easing rather than a sharp break. Chinese small green lentils, both conventional and organic, are broadly stable to slightly lower in a 1.06–1.14 EUR/kg window, reinforcing the signal of adequate global availability.

| Product | Origin | Latest price (EUR/kg, FOB) | 1–3 week trend |

|---|---|---|---|

| Lentils dried, Red football | Canada (Ottawa) | ≈ 2.37 EUR | Mildly lower |

| Lentils dried, Laird Green | Canada (Ottawa) | ≈ 1.60 EUR | Mildly lower |

| Lentils dried, Eston Green | Canada (Ottawa) | ≈ 1.51 EUR | Mildly lower |

| Lentils dried, small green (conv.) | China (Beijing) | ≈ 1.06 EUR | Stable/slightly lower |

🌦️ Weather & Short-Term Outlook

Favourable weather so far has supported good crop development for India’s summer green gram, and no major weather shock is currently priced into the market. With sowing up in Madhya Pradesh and Gujarat and harvest already started, the near-term supply outlook remains comfortable. Unless unexpected heatwaves or heavy pre-monsoon rains disrupt harvesting or quality, arrivals are set to increase further into late May and early June, preserving the current bearish tilt on the supply side.

Given this backdrop, the green gram market is likely to remain in a narrow trading band over the next three to four weeks. Prices are seen as too low relative to MSP to warrant a sharp further decline but too well supplied—via both farm output and government stocks—to sustain a strong move higher. This classic range-bound environment favours tactical buying on dips and disciplined selling into modest rallies, rather than attempts to anticipate a trend reversal.

📆 Trading Recommendations

- Importers and dal mills: Maintain need-based coverage, adding modest volumes on dips while the market trades at a discount to MSP, but avoid chasing short-lived rallies until post-harvest supply clarity improves.

- Producers: Consider staggered sales rather than aggressive holding, as large buffer stocks and rising arrivals limit near-term upside; use any price spikes toward MSP as opportunities to market additional volumes.

- Traders/speculators: Focus on range strategies, with tight risk management on both long and short positions. Aggressive long positioning appears premature before late-May arrival data and any potential policy adjustments are known.

📉 3-Day Price Directional View (EUR terms)

- Indian green gram (wholesale, MSP-discounted): Sideways to slightly softer, but no sharp fall expected over the next 3 days.

- Canadian lentils FOB (red and green types): Mildly soft bias, with further small euro-denominated easing possible if demand stays cautious.

- Chinese small green lentils FOB: Largely stable, with limited downside given already competitive euro prices.

Related posts:

Lentils Market: Indian Moong Under Pressure as Government Stocks Cap Upside

Lentils Market: Indian Moong Under Pressure as Government Stocks Cap Upside

Tighter Indian Supply Lifts Lentils While Imports Cap Upside

Tighter Indian Supply Lifts Lentils While Imports Cap Upside

Lentils Market Steady to Soft as Indian Green Gram Stocks Cap Upside

Lentils Market Steady to Soft as Indian Green Gram Stocks Cap Upside

Lentil Market Steady While Indian Black Gram Tightens Import Arbitrage

Lentil Market Steady While Indian Black Gram Tightens Import Arbitrage

Lentil Market Steady as Indian Black Gram Stays Soft but Well Supplied

Lentil Market Steady as Indian Black Gram Stays Soft but Well Supplied

Indian Chickpeas Steady as State Procurement Sets Floor, Imports Cap Upside

Indian Chickpeas Steady as State Procurement Sets Floor, Imports Cap Upside

Lentil Market Holds Steady as Indian Green Gram Stocks Cap Upside

Lentil Market Holds Steady as Indian Green Gram Stocks Cap Upside

Lentil Market Steady as Indian Green Gram Signals Comfortable Pulse Supply

Lentil Market Steady as Indian Green Gram Signals Comfortable Pulse Supply