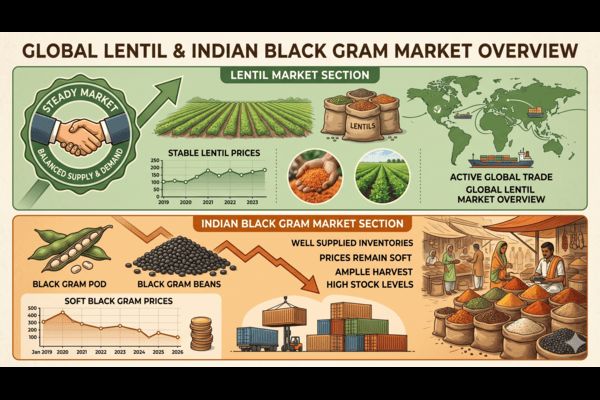

Indian black gram (urad), a key lentil-type pulse for global dal markets, is trading in a narrow, directionless range as increased imports from Myanmar meet seasonally weak domestic demand. Prices in India are currently below the government’s Minimum Support Price, and with buffer stocks relatively thin, the market remains well supplied yet cautious, especially on the processing and import side.

India’s wholesale and import markets show only marginal price moves across key consuming centres, with mills buying hand-to-mouth amid volatile Myanmar offers and steady Rabi arrivals. Expanded summer plantings in Madhya Pradesh and Gujarat, and harvests expected from late May, point to continued supply comfort and restrained price risks in the near term. For European lentil and dal users, this translates into a buyer-friendly environment for black gram ingredients over the next several weeks.

Exclusive Offers on CMBroker

Lentils dried

Red football

FOB 2.60 €/kg

(from CA)

Lentils dried

Laird, Green

FOB 1.77 €/kg

(from CA)

Lentils dried

Eston Green

FOB 1.67 €/kg

(from CA)

📈 Prices & Market Tone

Indian urad values had a mixed but overall soft week, with most benchmarks moving only a fraction. In Chennai, imported FAQ (fair average quality) urad for April–May shipment eased slightly to about USD 840/t CAD&F, while SQ grade softened to around USD 935/t. Domestic wholesale prices in Delhi and Guntur were broadly stable, with only marginal gains in the Chennai evening session, underscoring a lack of strong directional conviction.

At the same time, listed export offers for dried lentils remain steady. Converting the latest FOB prices approximately to EUR (assuming ~0.93 EUR per USD equivalent), Canadian red football lentils are around 2.42 EUR/kg, large green (Laird) at roughly 1.65 EUR/kg, and Eston green at about 1.55 EUR/kg. Chinese small green lentils sit near 1.14 EUR/kg (organic) and 1.07 EUR/kg (conventional), with no significant week-on-week moves. These levels are consistent with a calm, well-supplied global lentil complex.

🌍 Supply & Demand Balance

On the supply side, India is currently benefiting from steady Rabi urad arrivals in Andhra Pradesh, while summer crop sowings in Madhya Pradesh and Gujarat have expanded compared with last year. With harvest of these summer crops expected to start in late May, additional volumes should enter the market just as demand remains seasonally subdued, reinforcing a comfortable supply cushion.

Myanmar, India’s dominant origin for urad imports, is seeing alternating bouts of firmness and weakness in export prices, often described locally as a pattern of rapid ups and downs. This volatility is discouraging Indian mills from committing to large forward purchases; instead, they are buying only what they need for immediate processing. Despite this cautious purchasing strategy, the import pipeline from Myanmar is active enough to prevent any tightness, adding to the overall sense of balance and mild softness in the broader lentil and dal space.

📊 Fundamentals & Policy Context

A key structural feature of the current urad market is that spot wholesale prices in India are running below the Minimum Support Price of around USD 83.79 per quintal. This means farmers are not achieving the MSP in open market sales, and it partly explains why the central government has only accumulated a modest buffer stock of about 80,000 tonnes. Such a thin reserve limits the room for aggressive state-led market intervention if prices were to rally sharply later in the year.

For now, however, the combination of below-MSP prices, steady arrivals and ongoing imports signals an environment where upside price risk is capped in the short term. Without a clear demand-side trigger—such as festival-led buying or a sudden shift in consumer preferences—market participants expect urad and related lentil ingredients to trade sideways to slightly soft. International buyers of Indian black gram, including European dal and ready-meal manufacturers, can therefore secure coverage on a relatively comfortable basis.

📆 Short-Term Outlook & Weather

Looking over the next two to four weeks, the key drivers for urad and closely linked lentil products remain import costs from Myanmar and the pace of summer crop arrivals into Indian markets. With mills deliberately avoiding heavy stock-building, any short-lived firming in Myanmar offers is more likely to slow buying than to generate a sustained price rally. As summer harvests begin to flow from late May, domestic supply is poised to increase further, reinforcing a neutral-to-soft tone.

Weather in India’s major urad-growing belts is entering the pre-monsoon phase, and no widespread, acute stress has yet emerged that would immediately threaten near-term output. The main weather risk for the urad and lentil complex will come later with monsoon onset and distribution, but this lies outside the current one-month horizon. For now, most market participants are focused less on weather and more on logistics and import parity from Myanmar, alongside the subdued domestic demand profile.

🧭 Trading Outlook & Recommendations

- For European buyers: Use the current, supply-comfortable window to extend coverage for black gram-based ingredients one to three months forward, focusing on quality spreads between FAQ and SQ grades.

- For importers and traders: Maintain a cautious approach to forward purchases from Myanmar, aligning positions closely with confirmed demand, given the ongoing volatility in origin prices.

- For processors in India and abroad: Continue hand-to-mouth procurement in the very short term, but be prepared to lock in additional volumes if summer harvest arrivals confirm ample supply and keep domestic prices below MSP.

📍 3-Day Regional Price Indication (Directional, in EUR)

| Product / Origin | Location / Term | Current Level (approx. EUR/kg) | 3-Day Bias |

|---|---|---|---|

| Red football lentils (CA) | Ottawa, FOB | ≈ 2.42 | Sideways |

| Laird green lentils (CA) | Ottawa, FOB | ≈ 1.65 | Sideways / slightly soft |

| Eston green lentils (CA) | Ottawa, FOB | ≈ 1.55 | Sideways / slightly soft |

| Small green lentils (CN, conv.) | Beijing, FOB | ≈ 1.07 | Sideways |

| Small green lentils (CN, organic) | Beijing, FOB | ≈ 1.14 | Sideways |

Related posts:

Lentil Market Holds Steady as Indian Green Gram Stocks Cap Upside

Lentil Market Holds Steady as Indian Green Gram Stocks Cap Upside

Lentil Market Steady as Indian Green Gram Signals Comfortable Pulse Supply

Lentil Market Steady as Indian Green Gram Signals Comfortable Pulse Supply

Chickpeas Stay Sub-MSP but Attractive for EU Buyers as India Remains Well Supplied

Chickpeas Stay Sub-MSP but Attractive for EU Buyers as India Remains Well Supplied

Global Lentil Market Steady as Indian Green Gram Signals Structural Oversupply

Global Lentil Market Steady as Indian Green Gram Signals Structural Oversupply

Lentil Market Steady as Indian Green Gram Oversupply Caps Upside

Lentil Market Steady as Indian Green Gram Oversupply Caps Upside

Indian Lentil Market Steadies as Canadian Cargo Tests Tight Domestic Supply

Indian Lentil Market Steadies as Canadian Cargo Tests Tight Domestic Supply

Lentil prices in China steady to slightly firmer as energy shock lifts costs

Lentil prices in China steady to slightly firmer as energy shock lifts costs

Lentils market steadies as Indian green gram glut caps upside

Lentils market steadies as Indian green gram glut caps upside