The European Union’s latest steps toward implementing its new trade framework with the United States, including preferential access for a wide range of U.S. agricultural products, coincide with a marked demand slowdown in the American pecan sector. Together, these developments are set to reshape price dynamics and procurement strategies in the transatlantic tree‑nut trade, particularly for European buyers. While policy still faces final ratification hurdles, nut and dried-fruit traders are already reassessing forward coverage and origin mix.

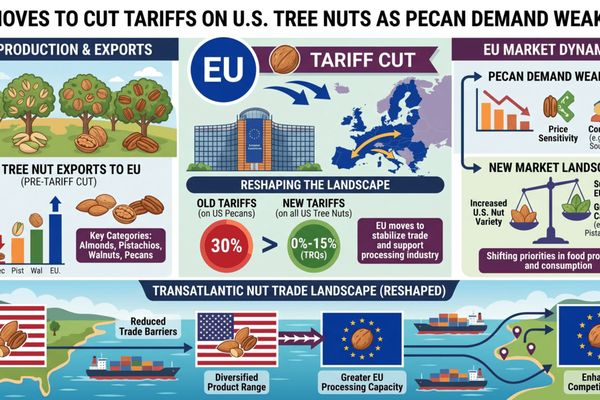

U.S. pecan shipments in March 2026 fell 21% year on year even as inventories climbed above historical averages, according to newly released American Pecan Council data. At the same time, EU institutions have moved forward with legislation to implement a broad EU–US trade agreement that will phase in tariff reductions and quota preferences for U.S. seafood and agricultural products, including tree nuts. The intersection of softer U.S. demand, ample supply and improving EU market access points to a more competitively priced U.S. offer into Europe over the coming marketing months.

Introduction

On 26 March 2026, the European Parliament adopted implementing legislation for a new EU–US trade agreement that, once fully ratified, will eliminate most tariffs on U.S. industrial products and grant preferential market access to selected U.S. agricultural exports. Draft texts and accompanying mandates explicitly reference tariff cuts and new tariff‑rate quotas for several agri‑food lines, including tree nuts. Although trilogue negotiations with the Council and Commission are still required, the direction of policy is clear: lower EU border protection for many U.S. farm goods.

In parallel, the U.S. pecan industry has entered the second half of the 2025/26 marketing year with a pronounced demand problem. March 2026 shipments totalled just over 25 million pounds in in‑shell equivalent, down 21% from March 2025, while end‑March inventories increased and now sit slightly above their five‑year average. Europe remains the single largest export destination for U.S. pecans, implying that any combination of weaker consumer demand and policy‑driven tariff changes will be quickly reflected in transatlantic trade flows.

🌍 Immediate Market Impact

In the near term, the prospect of reduced EU tariffs on U.S. tree nuts is likely to reinforce already bearish price sentiment in the American pecan market. With shipments lagging and inventories building, U.S. handlers have limited leverage to resist more aggressive pricing into Europe, especially if lower duties further narrow the landed‑cost gap versus competing origins such as Mexico and South Africa.

For European buyers, the combination of softer U.S. fundamentals and potential tariff relief translates into improved buying conditions for the 2026/27 contracting cycle. The risk, however, is elevated price volatility: the broader EU–US trade relationship is being buffeted by a separate set of U.S. tariff initiatives, including a 10–15% global import surcharge that has injected uncertainty into trade policy and currency‑adjusted price formation.

📦 Supply Chain Disruptions

From a logistics perspective, the new EU framework is not expected to create immediate physical bottlenecks, but it may alter the utilisation of existing supply chains. Preferential quotas and reduced duties will likely be channelled through established EU container ports handling high‑value agri‑food imports, notably Rotterdam, Antwerp-Bruges, Hamburg and Mediterranean gateways serving confectionery and bakery clusters.

Administrative changes could be more material than physical ones in the short run. Traders will need to adjust customs coding, certificate management and quota allocation strategies to capture lower duty rates, especially where tariff‑rate quotas for tree nuts or mixed snack products apply. This comes on top of existing EU food‑safety controls for nuts and dried fruit, including reinforced aflatoxin checks on certain origins, which continue to complicate sourcing decisions across the nut complex.

📊 Commodities Potentially Affected

- Pecans (U.S. origin) – Weakened U.S. shipments and above‑average inventories, combined with improved EU market access, point to continued downside pressure on export prices and more aggressive offers into Europe.

- Almonds and other U.S. tree nuts – Inclusion of “tree nuts” among products earmarked for preferential treatment suggests incremental competitiveness versus non‑U.S. origins, especially in EU snack and confectionery applications.

- Processed nut ingredients (pralines, pastes, mixes) – Lower input costs from U.S. nuts could filter through into semi‑processed products supplied to EU food manufacturers, potentially reshaping tender outcomes for 2027 delivery.

- Competing origins (Mexico, South Africa, Australia) – Depending on final tariff schedules, third‑country suppliers may face relative margin compression in the EU as U.S. nuts gain a duty advantage and widen discounts to maintain throughput.

🌎 Regional Trade Implications

Europe currently absorbs roughly half of U.S. pecan exports in a typical March shipping month, making it the pivotal outlet for clearing U.S. surpluses. As EU tariffs ease, U.S. exporters are positioned to defend or even expand market share in key consuming countries such as Germany, the Netherlands, France and the UK (via inward processing for re‑exports), provided consumer demand stabilises.

On the losing side, alternative origins supplying Europe could see volumes capped or prices forced lower to stay competitive. However, if the wider transatlantic trade relationship deteriorates—through additional U.S. tariff actions or EU counter‑measures in other sectors—uncertainty could dampen investment in origin‑specific processing and storage capacity on both sides. In that scenario, some EU buyers may choose to diversify sourcing further into non‑U.S. origins despite formal tariff preferences.

🧭 Market Outlook

Over the next two to four months, pecan fundamentals point to sustained supply pressure and a buyer’s market. Unless demand in the U.S. confectionery and bakery sectors rebounds or export offtake accelerates, particularly from Europe and the Middle East, sellers will struggle to lift prices from current levels. The prospective EU tariff cuts only reinforce this dynamic by making lower U.S. offers more attractive on a landed‑duty basis.

Traders will closely monitor three variables: the timing and final shape of EU–US implementing legislation, any fresh U.S. tariff announcements that could provoke EU retaliation, and updated shipment and inventory data from the American Pecan Council. A clearer policy environment could unlock deferred purchasing, but ongoing trade‑policy volatility argues for flexible coverage strategies.

CMB Market Insight

The convergence of weaker U.S. pecan demand, comfortable inventories and impending EU tariff reductions is strategically significant for agricultural commodity markets. For at least the coming marketing year, the transatlantic tree‑nut trade looks set to tilt in favour of European buyers, who can leverage both fundamentals and policy to secure more competitive pricing and favourable contract terms.

U.S. nut exporters, by contrast, face a dual challenge: managing downside price risk in a soft pecan market while navigating an unpredictable U.S. tariff environment that could spill over into broader EU–US relations. Risk‑adjusted strategies—including diversified destination portfolios, optionality in incoterms and active use of forward and options structures—will be essential for both sides as policy and market signals continue to evolve.

Related posts:

U.S. Trade Deficit Widens in March as Imports and Exports Hit Records – Mixed Signals for Agri-Food Trade

U.S. Trade Deficit Widens in March as Imports and Exports Hit Records – Mixed Signals for Agri-Food Trade

Indian GM-Free Coalition Challenges US-India Trade Talks on DDGs and Soybean Oil

Indian GM-Free Coalition Challenges US-India Trade Talks on DDGs and Soybean Oil

US Tariff Refunds Create Historic Cash Reversal for Importers, Reshaping Cost Structures Across Supply Chains

US Tariff Refunds Create Historic Cash Reversal for Importers, Reshaping Cost Structures Across Supply Chains

Poland Moves to Block EU–Mercosur Deal as Fertiliser Tariff Shift Looms, Raising Questions for Grain and Livestock Markets

Poland Moves to Block EU–Mercosur Deal as Fertiliser Tariff Shift Looms, Raising Questions for Grain and Livestock Markets

China’s Zero-Tariff Opening to 53 African Countries Poised to Reshape Agricultural Trade Dynamics

China’s Zero-Tariff Opening to 53 African Countries Poised to Reshape Agricultural Trade Dynamics

EU Extends Licensing and Quotas on Ukrainian Sunflower Seed Exports to Neighbouring EU States, Reshaping Black Sea Oilseed Trade

EU Extends Licensing and Quotas on Ukrainian Sunflower Seed Exports to Neighbouring EU States, Reshaping Black Sea Oilseed Trade