The United Arab Emirates’ decision to leave OPEC from 1 May 2026 removes the cartel’s third‑largest producer from its quota system, weakening the group’s ability to coordinate supply and manage prices. In the very short term, export constraints via the closed Strait of Hormuz are capping physical flows, but forward curves and hedging demand are already adjusting to a structurally looser OPEC discipline. For energy‑intensive agrifood supply chains, this marks a pivotal shift in long‑term fuel cost and freight risk.

Markets now face a dual reality: immediate supply remains throttled by the Gulf shipping crisis, yet the post‑war outlook points to a potentially more competitive production environment led by an unconstrained UAE. This combination is likely to increase price volatility across the oil complex, with knock‑on effects for diesel, bunker fuel, fertilizer feedstocks and global food logistics.

Introduction

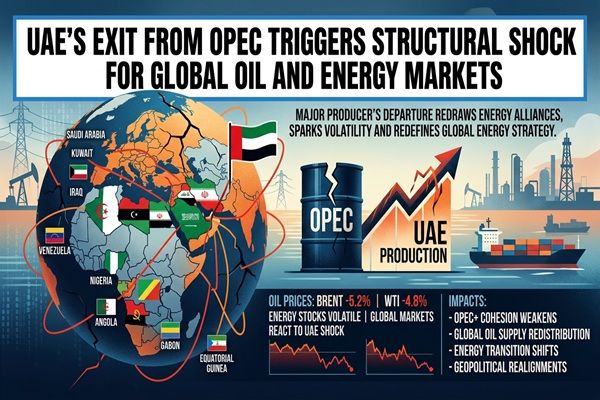

On 28 April 2026, the UAE announced it will withdraw from the Organization of the Petroleum Exporting Countries and the wider OPEC+ group effective 1 May, ending nearly six decades of membership. The move strips OPEC of a producer accounting for roughly 3–4% of global oil output and one of the few members capable of quickly ramping production.

The decision comes amid a war involving Iran and the effective closure of the Strait of Hormuz, which has already forced Gulf exporters, including the UAE and Saudi Arabia, to curtail shipments. While the immediate effect on seaborne volumes is limited by these constraints, the group’s weakened cohesion is a structural break for global energy markets that underpins fuel and freight cost assumptions across agricultural commodity supply chains.

🌍 Immediate Market Impact

Financial markets reacted quickly: reports indicate oil prices eased following the announcement, as traders priced in the prospect of a more competitive supply landscape once Gulf exports normalize. At the same time, analysts highlight that OPEC’s diminished ability to deploy spare capacity in a coordinated fashion raises the risk of sharper price swings in response to future demand or geopolitical shocks.

In the near term, however, the war and Hormuz bottleneck mean the UAE cannot materially increase exports despite being freed from quotas; Gulf producers collectively have significant idled capacity that cannot reach market. For energy‑dependent agrifood traders, this translates into a market where headline prices may soften modestly on sentiment, but physical availability and freight risks in key east–west routes remain constrained.

📦 Supply Chain Disruptions

The closure or severe disruption of the Strait of Hormuz continues to be the primary logistical choke point, limiting crude and product flows from the Gulf regardless of the UAE’s policy shift. Several analyses note that any incremental UAE supply is effectively trapped until shipping lanes normalize, reinforcing tightness in regional bunker markets and complicating voyage planning for bulk and reefer carriers serving Asia, the Middle East and Europe.

Looking beyond the immediate crisis, the UAE’s exit introduces new uncertainty into long‑term supply coordination. With Abu Dhabi targeting higher production capacity (around 5 million barrels per day over time) and no longer bound by OPEC quotas, future ramp‑ups could pressure prices just as other producers invest in upstream capacity. This complicates investment and hedging decisions for fertilizer plants, biofuel producers and food manufacturers whose margins are tightly linked to diesel and gas‑derived inputs.

📊 Commodities Potentially Affected

- Crude oil (Brent, Dubai, Oman) – Directly affected by a structurally weaker OPEC, with potential for looser supply discipline once Hormuz reopens and UAE output rises relative to quotas.

- Refined products (diesel, marine gasoil, fuel oil) – Freight, trucking and agricultural machinery fuels face elevated volatility; a future UAE‑led supply increase could cap prices but also trigger sharper cycles.

- Bunker fuel for dry bulk and container shipping – Energy costs for grain, oilseed, sugar and meat shipments will reflect changing expectations for Gulf export availability and global refining runs.

- Nitrogen fertilizers (urea, UAN, ammonia) – Oil and associated gas price expectations feed into nitrogen production economics and freight; any sustained downward pressure on crude post‑war would ease cost curves, while volatility complicates forward purchases.

- Biofuel feedstocks (vegetable oils, sugar, corn) – Shifts in diesel and gasoline pricing influence biofuel mandates and discretionary blending, altering demand for crops used in biodiesel and ethanol.

🌎 Regional Trade Implications

Once Hormuz constraints ease, a quota‑free UAE is likely to push more crude eastward to Asia, reinforcing the Gulf–Asia energy corridor and intensifying competition with Saudi, Iraqi and Russian barrels. This could benefit major importers such as India and China through improved supply options and potentially narrower differentials, though at the cost of higher price volatility.

Atlantic Basin producers, including West African and Latin American exporters, may face tighter margins if additional Gulf supply weighs on medium‑sour benchmarks. For agricultural exporters in those regions, cheaper fuel could support competitiveness on delivered‑CFR terms, but only if logistics bottlenecks in the Gulf do not spill over into broader shipping disruptions or insurance premia.

🧭 Market Outlook

In the short term, traders should treat the UAE’s exit as primarily a forward‑curve and risk‑premium story rather than an immediate physical shock: constrained exports mean spot balances remain dominated by war‑related outages, but expectations for post‑war supply are shifting towards greater non‑OPEC‑disciplined volumes.

Over the next 6–24 months, key variables to monitor include the reopening of Hormuz, UAE progress on production expansion, any compensatory strategy from the remaining OPEC+ members, and policy shifts around energy transition and biofuels. Agricultural and food‑industry players may find opportunities to lock in lower forward fuel and freight costs during periods of price weakness, but should pair this with robust options strategies or diversified index hedges to manage the heightened volatility regime.

CMB Market Insight

The UAE’s withdrawal from OPEC is less about today’s tanker loadings and more about tomorrow’s price architecture. For commodity markets, it signals a transition from a tightly quota‑managed crude system towards a more fragmented, competitive landscape in which Gulf spare capacity is no longer deployed under a single cohesive framework.

Energy‑intensive agricultural value chains—from fertilizer production and grain exports to cold‑chain meat and dairy logistics—must now assume structurally higher oil‑price volatility, even if average levels moderate over time. Strategic priorities for market participants include reassessing long‑term fuel hedging policies, stress‑testing freight and input cost scenarios, and closely tracking Gulf shipping and OPEC+ cohesion as leading indicators for the next phase of global commodity price cycles.

Related posts:

Middle East War Tightens Strait of Hormuz, Driving Energy Shock and Food Cost Pressures

Middle East War Tightens Strait of Hormuz, Driving Energy Shock and Food Cost Pressures

Brazil Launches B20 Diesel Blend Tests, Signalling Structural Shift for Soy Oil and Biodiesel Markets

Brazil Launches B20 Diesel Blend Tests, Signalling Structural Shift for Soy Oil and Biodiesel Markets

Tight Vegetable Oil Complex Lifts Sunflower Prices Amid Energy Shock

Tight Vegetable Oil Complex Lifts Sunflower Prices Amid Energy Shock

Strait of Hormuz Conflict Triggers Fertilizer Supply Shock and Raises Global Crop Cost Risks

Strait of Hormuz Conflict Triggers Fertilizer Supply Shock and Raises Global Crop Cost Risks

Strait of Hormuz Reopens Under Ceasefire, Easing Acute Stress on Global Energy and Commodity Flows

Strait of Hormuz Reopens Under Ceasefire, Easing Acute Stress on Global Energy and Commodity Flows

Strait of Hormuz Blockade Triggers Fuel Shock and Global Freight Rate Surge

Strait of Hormuz Blockade Triggers Fuel Shock and Global Freight Rate Surge