Australia’s surprise March 2026 trade deficit, its first in more than eight years, underscores how the Iran conflict–driven fuel price shock is reshaping trade balances, freight costs and margin structures across key commodity export sectors. A sharp surge in fuel imports and softer resource exports have important implications for agricultural exporters, processors and international buyers relying on Australian-origin supplies.

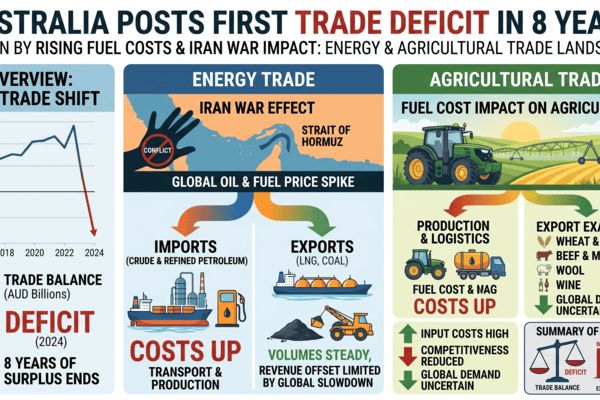

The Australian Bureau of Statistics reported a goods trade deficit of AUD 1.84 billion in March, versus expectations for a solid surplus, as imports jumped 14.1% month-on-month and exports fell 2.7%. The data highlight a steep increase in crude and refined fuel imports amid global oil prices that have spiked above USD 100–120 per barrel during the Strait of Hormuz crisis linked to the Iran war, while coal and LNG exports underperformed and commodity shipments softened.

Headline

War-Driven Fuel Surge Pushes Australia into First Trade Deficit Since 2017, Raising Costs for Commodity Supply Chains

Introduction

March 2026 trade data show Australia recording an unexpected goods trade deficit of AUD 1.84 billion, the country’s first monthly shortfall since December 2017, after a long period of sizeable surpluses underpinned by minerals, energy and agricultural exports. Imports were pulled higher by capital goods and a pronounced increase in crude petroleum and gasoline purchases, while export values softened on weaker volumes of several key commodities.

The deterioration comes against the backdrop of the Iran war and the 2026 Strait of Hormuz crisis, which have driven one of the fastest oil price rises in modern history and pushed benchmark crude briefly as high as about USD 126 per barrel. The spike has lifted global fuel and freight costs and exposed structural vulnerabilities in fuel-importing economies, including Australia, which imports much of its refined product despite being a major energy exporter.

🌍 Immediate Market Impact

The shift to deficit is being driven by a war-related fuel import shock: imports of crude petroleum, gasoline and related products climbed sharply in March, reflecting both higher volumes and higher unit prices. Market commentary points to inventory front-loading by refiners and fuel distributors seeking to hedge against further supply disruptions through the Strait of Hormuz and ongoing volatility in oil benchmarks.

For commodity markets, the immediate impact is twofold. First, higher domestic fuel and freight costs are raising cost bases for Australian exporters of grains, oilseeds, beef, sugar and horticultural products, at a time when international buyers remain price-sensitive. Second, any persistent margin squeeze may curb export offers or accelerate price pass-through in upcoming tenders, particularly for bulk agricultural cargos shipped to Asia and the Middle East.

📦 Supply Chain Disruptions

While Australia’s ports remain operational, the combination of higher bunker fuel prices, elevated insurance premia for routes linked to the Gulf, and increased crude and product import runs is tightening domestic logistics capacity. The jump in fuel shipments, together with strong imports of data centre and capital equipment, is contributing to heavier throughput at key container and energy terminals.

On the export side, coal and LNG volumes were weaker than a year earlier, with LNG shipments also affected by earlier cyclone-related disruptions. This meant Australia was unable to fully capitalise on elevated spot energy prices, even as its import fuel bill ballooned. Gold exports provided some offset thanks to record-high bullion prices, but not enough to prevent the overall swing into deficit.

For agricultural exporters, higher road, rail and port handling costs are feeding through the supply chain. Rising diesel and gasoline prices increase on-farm operating expenses and domestic haulage costs from inland production regions to export terminals, narrowing producer and trader margins and potentially altering origin competitiveness into Asian and European markets.

📊 Commodities Potentially Affected

- Wheat and Coarse Grains – Export margins are pressured by higher diesel and ocean freight costs, which may lift Australian FOB offers relative to Black Sea and North American origins in upcoming tenders.

- Beef and Livestock – Fuel-intensive transport from feedlots and grazing regions to processing plants and ports raises per-head logistics costs, with knock-on effects for boxed beef export prices into Asia and the US.

- Sugar – Cane hauling and milling are energy-intensive; higher fuel and power costs may tighten margins for mills and traders and support a firmer floor under Australian export prices.

- Horticultural Products – Refrigerated transport and cold-chain logistics face rising input and bunker costs, challenging the competitiveness of long-haul exports to North Asia and the Middle East.

- LNG and Thermal Coal – Weaker March volumes and earlier weather disruptions limited upside from high global energy prices, but any subsequent recovery in shipments will be closely watched by freight markets.

- Gold – Elevated gold prices have supported export receipts and partially cushioned the trade balance, but this offers limited direct relief to physical agricultural markets.

🌎 Regional Trade Implications

In the Asia–Pacific region, higher Australian fuel import costs and freight rates may gradually redistribute some demand for grains and beef toward origins with lower logistics costs or stronger currency advantages. Black Sea wheat and South American soy and corn could gain incremental market share in price-sensitive destinations in Southeast Asia if Australian offers widen sufficiently.

Conversely, Australia remains a critical supplier of quality wheat, barley, beef and sugar to North and Southeast Asia, and many buyers value its reliability and food-safety profile. Importers may accept higher Australian price levels in exchange for supply security, particularly while Middle East–related disruptions continue to cloud shipping through the Gulf and complicate alternative sourcing from that region.

The broader Iran war fuel crisis is also prompting some regional reconfiguration of energy and refined product flows, with Asian refiners and trading hubs such as Singapore adjusting sourcing patterns. This could, over time, influence bunker availability and pricing at Australian ports, with indirect effects on freight costs for bulk agricultural cargoes.

🧭 Market Outlook

Over the next 30–90 days, Australia’s trade balance will remain sensitive to the path of global oil prices and any further escalation or de-escalation in the Iran conflict. If fuel import volumes stay elevated due to continued inventory building and crude remains near recent highs, the pressure on the trade account and on domestic fuel prices is likely to persist, maintaining upward pressure on logistics and input costs for commodity exporters.

In the medium term, a partial normalisation of oil prices or an easing of geopolitical tensions would provide relief to freight and input markets. At the same time, a recovery in LNG and coal export volumes could help rebuild Australia’s trade surplus and bolster shipping demand. Traders will closely monitor FOB price spreads between Australian and competing origins, freight differentials into key Asian destinations, and any evidence of demand rationing by importers confronted with higher landed costs.

CMB Market Insight

Australia’s March 2026 trade deficit marks a notable inflection point in the global commodity landscape: a traditionally surplus energy and resource exporter experiencing war-driven fuel import stress at the same time that export volumes are underperforming. For agricultural and food-industry stakeholders, the key takeaway is not the deficit itself, but the structural rise in fuel and freight costs feeding into Australian supply chains.

In this environment, Australian-origin commodities are likely to command a higher cost base, and traders should reassess pricing, hedging and origin strategies for the remainder of 2026. Close tracking of oil and bunker markets, Australian logistics costs and cross-origin price spreads will be critical for importers, exporters and processors managing exposure to this evolving trade shock.